doi: 10.56294/dm2023203

ORIGINAL

Balanced scorecard in the business development of MSMEs in the district of San Vicente de Cañete

Balanced Scorecard en el desarrollo empresarial de las MiPYMES del distrito de San Vicente de Cañete

Rayda Villalobos-Castro1 ![]() *, Segundo Ríos-Ríos1

*, Segundo Ríos-Ríos1 ![]() * , Fernando

Ochoa-Paredes1

* , Fernando

Ochoa-Paredes1 ![]() *, Miguel Vargas-Tasayco1

*, Miguel Vargas-Tasayco1 ![]() *, Yrene Uribe-Hernandez1

*, Yrene Uribe-Hernandez1 ![]() *

*

1Universidad Nacional de Cañete. Facultad de Administración de Empresas. Ica, Perú.

Cite as: Villalobos-Castro R, Ríos-Ríos S, Ochoa-Paredes F, Vargas-Tasayco M, Uribe-Hernandez Y. Balanced scorecard in the business development of MSMEs in the district of San Vicente de Cañete. Data and Metadata. 2023;2:203. https://doi.org/10.56294/dm2023203

Submitted: 14-08-2023 Revised: 31-10-2023 Accepted: 29-12-2023 Published: 30-12-2023

Editor: Prof.

Dr. Javier González Argote ![]()

ABSTRACT

Introduction: This research was carried out on the topic: “Balanced scorecard in the business development of MSMEs in the district of San Vicente de Cañete, 2021”.

Objective: Determine the influence of the balanced scorecard on the business development of MSMEs in the province of Cañete, 2021, so that the balanced scorecard indicators are considered the choice of MSMEs for an improvement in decision making.

Method: In this scenario, an applied methodology was developed, with a quantitative approach, a non-experimental, transversal and correlational design. A questionnaire was used as a survey of 68 managers of MSMEs, which was made up of 23 questions on a Likert scale, these being validated with expert judgment.

Results: The results achieved allowed us to confirm the hypotheses raised that the balanced scorecard has a significant influence on the business development of MSMEs in the province of Cañete, 2021, as well as the secondary hypotheses were confirmed.

Conclusions: The same ones that stated that the balanced scorecard significantly influences economic profitability, product quality, resource optimization and innovation in MSMEs in the province. de Cañete, 2021.

Keywords: Balanced Scorecard; Business Development; Influence.

RESUMEN

Introducción: La presente investigación se realizó sobre el tema: “Balanced scorecard en el desarrollo empresarial de las MiPYMES del distrito de San Vicente de Cañete, 2021”.

Objetivo: Determinar, cuál es la influencia del balanced scorecard en el desarrollo empresarial de las MiPymes de la provincia de Cañete, 2021, para que los indicadores del balanced scorecard sean considerados como la elección de las MiPymes para una mejora en la toma de decisiones.

Método: En este escenario se desarrolló una metodología aplicada, con un enfoque cuantitativo, un diseño no experimental, transversal y de nivel correlacional. Se utilizó un cuestionario a modo de encuesta a 68 directivos de MiPymes, el cual estuvo conformado por 23 preguntas en escala Likert, siendo estas validadas con juicio de expertos.

Resultados: Los resultados alcanzados permitieron confirmar las hipótesis planteadas en que el balanced scorecard tiene una influencia significativa en el desarrollo empresarial de las MiPYMES en la provincia de Cañete, 2021, así como también se confirmaron las hipótesis secundarias.

Conclusiones: Las mismas que plantearon que el balanced scorecard influye significativamente en la rentabilidad económica, la calidad del producto, la optimización de recursos y la innovación en las MiPYMES de la provincia. de Cañete, 2021.

Palabras clave: Balanced Scorecard; Desarrollo Empresarial; Influencia.

INTRODUCTION

Bada Carbajal & Rivas Tovar (1), mentions that Micro, Small and Medium Enterprises (MSMEs) have proven to be a determining factor in the economic development of each country at different times and places, since they have been the dominant factor of the economy in terms of employment, investment and production.

At the global level, according to Valdés Díaz de Villegas & Sánchez Soto(2) he states that "this type of companies represent around 90 % of existing companies globally, employ 50 % of the workforce and participate in the creation of 50 % of world GDP".

In the United States, for example, according to the research of Valdés Díaz de Villegas & Sánchez Soto(2) on MSMEs in a global context, it states that "in the United States, 99 % of companies are MSMEs, and provide approximately 75 % of net new jobs, which are generated each year in the country's economy; This type of company employs 50,1 % of the private workforce".

On the other hand, MSMEs in Latin America according to Dini & Stumpo(3) represent 99,5 % of the companies in the region and the vast majority are microenterprises (88,4 % of the total).

Such is the case of Ecuador, for example, the MSME sector represents more than 95 % of the business structure, the most important economic sectors of the economy are: trade, service, manufacturing industry, mining and extraction, construction, agriculture, livestock, forestry and fishing, hence the importance of knowing their growth and sustainability.(4)

In Colombia, according to Álvarez Contreras & Jiménez Lyonz.(5) points out the following: our regions are mainly populated by MSMEs, which make an invaluable contribution to the country's economic activity, representing 99,5 % of the business fabric, contributing 67 % of total employment and 28 % of gross domestic product. However, a study by Bravo García et al. (6) concludes by stating that the problems with the greatest impact that MSMEs have in Colombia are administrative, financial, production, macroeconomic, personal, formalization and with workers.

In Peru, according to INEI(7) reports that: "micro, small and medium-sized enterprises (MSMEs) have represented around 99,3 % of total companies during the last five years; with an average annual growth rate of 7,0 %"

However, Arasti et al.(8) one of the main problems for MSMEs is the lack of resources, such as employees, business management skills of the owner, as well as stability and financial security. Peru is at a disadvantage compared to developed countries, which is why, in recent years, the state has formulated and implemented several state policies for MSMEs.(9).

That is why in the present research we focused on studying what is the influence of the Balanced Scorecard as an alternative to improve the business development of MSMEs in the jurisdiction of San Vicente de Cañete, given that these mostly have inadequate business management that occurs due to inadequate decision making, product of the ignorance of clear strategies that help to expand the panorama and internal and external reality of the company, mostly those who direct them are enterprising people with desires to excel but without the knowledge due to an adequate administration, it is expected that this research work allows an adequate planning in the MSMEs, applying each of its indicators and guiding them towards the generation of profitability, helping entrepreneurs to make adequate and timely decisions that contribute to increase their profits, promoting better business development systems that allow a more dynamic and comprehensive understanding in the MSME sector, these being economic units that contribute: generating employment, contributing to GDP, reducing poverty, encouraging entrepreneurship and contributing to economic growth.

That is why as a General Problem it was raised: How does the Balanced Scorecard influence the business development of MSMEs in the province of Cañete, 2021? , as well as the Specific Problems: 1) How does the Balanced Scorecard influence the economic profitability of MSMEs in the province of Cañete, 2021? , 2) How does the Balanced Scorecard influence the product quality of MSMEs in the province of Cañete, 2021? , 3) How does the Balanced Scorecard influence the optimization of resources of MSMEs in the province of Cañete, 2021? , and (4) How does the Balanced Scorecard influence the innovation of MSMEs in the province of Cañete, 2021? .

In addition, as a General Objective, it was proposed: Determine, what is the influence of the Balanced Scorecard on the business development of MSMEs in the province of Cañete, 2021. , as well as Specific Objectives: 1) Determine if the Balanced Scorecard influences the economic profitability of MSMEs in the province of Cañete, 2021., 2) Determine if the Balanced Scorecard influences the product quality of MSMEs in the province of Cañete, 2021., 3) Determine if the Balanced Scorecard influences the optimization of resources of MSMEs in the province of Cañete, 2021., and 4) Determine if the Balanced Scorecard influences the innovation of MSMEs in the province of Cañete, 2021.

As a General Hypothesis it was proposed: The Balanced Scorecard significantly influences the business development of MSMEs in the province of Cañete, 2021, as well as Specific Hypotheses: 1) The Balanced Scorecard significantly influences the economic profitability of MSMEs in the province of Cañete, 2021. , 2) The Balanced Scorecard significantly influences the product quality of MSMEs in the province of Cañete, 2021., 3) The Balanced Scorecard significantly influences the optimization of resources of MSMEs in the province of Cañete, 2021., and 4) The Balanced Scorecard significantly influences the innovation of MSMEs in the province of Cañete, 2021.

Academic justification

In this research work, the following is fulfilled:

· Regulation to grant the academic degree of bachelor and professional title at the National University of Cañete, according to resolution of the organizing committee No. 180-2021-UNDC.

· Line of research of the UNDC, according to resolution of the organizing committee No. 096-2016-UNDC.

· University Law No. 30220.

Theoretical justification

This work is of utmost importance since it originates to know the influence of the Balanced Scorecard as an alternative to improve the business development of MSMEs in the jurisdiction of San Vicente de Cañete, it is expected that this research will contribute to adequate planning in microenterprises, helping microentrepreneurs to make adequate and timely decisions that help increase their profits.

Technical justification

Currently there are many MSMEs in the area of San Vicente de Cañete, mainly led by entrepreneurs who want to succeed, but do not have the appropriate knowledge to manage properly, with Balanced Scorecard, aimed at better business development, it is intended to improve development systems that allow a more dynamic and comprehensive understanding of the field of MSMEs, this tool will help manage the company's strategy allowing a better understanding of its objectives in all areas, as well as carrying out systematic, periodic strategic reviews and receiving feedback.

Economic justification

The relevance of this research is of an economic nature. The MSMEs of the authority of San Vicente de Cañete constitute the unit in which the application of the Balanced Scorecard model will be experienced, applying each of its indicators and guiding them towards the generation of profitability, thus helping with each of the companies and serving as a guide for others.

Social justification

It has social relevance because the MSMEs of the jurisdiction of San Vicente de Cañete constitute economic units that contribute: generating employment, contributing to GDP, reducing poverty, encouraging entrepreneurship and contributing to economic growth, it is intended to contribute to the business development of MSMEs, providing them with practical strategies that will help to implement clear horizons, resulting in sustainable development through strategic plans guaranteeing its prolongation and contribution to society.

Methodological justification

In this research we want to follow the guidelines developed in the scientific research process, which include formulating questions, objectives, and hypotheses, to obtain a probable knowledge about the influence of the Balanced Scorecard on the business development of MSMEs in the jurisdiction of San Vicente de Cañete 2021.

Background

Mendoza Mieles et al.(4) in their scientific article, states that currently MSMEs are the most productive sector in a country since they influence job creation and economic movement, in addition, it is considered a priority for economic growth, however, these MSMEs find it a challenge to grow, develop, and above all stay in the market. For this research, companies with less than 200 employees were considered as MSMEs, a documentary and descriptive research was used, reaching the following conclusion: there are barriers that prevent the emergence and growth of the business, one of which is the lack of strategic planning, innovation, liquidity, weak knowledge management, government support, and certain business models that do not allow to take advantage of presence opportunities in emerging markets for greater performance and brand positioning. Therefore, an entrepreneur must acquire and develop a set of skills that help him to have a vision of the future.

Mendez & Mendez(10) in its scientific article, analyzes based on a literary research in sources of high impact to the Balanced Scorecard from different perspectives, reaching the following conclusions: a) BSC is applicable to all types of organizations because it can be easily adapted without sacrificing the ability to improve efficiency, b) the implementation of the BSC enables and promotes the participation of all employees, improves interpersonal relationships and communication at the entire hierarchical level, c) as a result of the COVID-19 pandemic, all economies have been affected, generating unemployment, completely changing consumption trends, worst of all, some companies had to close, so there is a need for a tool that helps increase the productivity of the company and this support tool is the BSC.

Colimba Farinango(11) in his undergraduate thesis, where the main objective was the application of the BSC in the business management of the mentioned company and as secondary objectives: diagnose the current situation of the company, diagnose the influence of the BSC in business management through a correlation analysis, and finally, to evaluate the BSC's strategic perspectives through management indicators. A quantitative and qualitative research is applied, of correlational descriptive alcande, of non-experimental, cross-sectional and longitudinal design, had a sample of 317 people and applied the techniques of survey and interview; As an instrument I use the questionnaire; finally I conclude that the most efficient tool is the BSC since it allows to visualize the objectives of the organization. Evidence of the existence of internal and external barriers that affect the organization when diagnosing the situation of the company was found, on the other hand when performing the analysis of the incidence of the BSC in business management through the statistical test of Pearson's Coefficient it was confirmed that, if there is a positive relationship between these variables. Finally, it recommends the implementation of the BSC in order to use the objectives and strategies to be used.

Jiménez Silva et al.(12) in their scientific article a theoretical-scientific research work whose general objective was to analyze the connection between organizational knowledge management and the perspectives of the BSC as a key factor in the organizational innovation of SMEs based on two unique objectives, being these: documenting research on knowledge management, the BSC perspective and innovation in the current context; and the role of the BSC perspective in knowledge management for SME innovation. Finally, after exhaustively researching various documents, I conclude that the perspectives of the BSC guide how to properly manage intellectual capital to achieve business innovation, and thus obtain a competitive advantage.

Delgado Requejo(13), in his master's thesis aims to propose the Balanced Scorecard to improve the business management of the company CACIDEP S.A.C., Cajamarca 2021, where I use basic research, mixed, descriptive-prospective, with non-experimental-transversal design, prospective under the hypothetical-deductive method using an intentional non-probabilistic sampling. The population and sample of the research in question consists of 14 employees to whom a survey with 14 questions was applied. Finally, it assigns the following proposal: The Balanced Scorecard aims to help CACIDEP S.A.C. improve the management of the company by combining strategic objectives with business philosophy, thus achieving total control over the organization through management indicators.

Colareta Arriola(14) in his undergraduate thesis, establishing as an objective to demonstrate if the Balanced Scorecard influences the business management of the MSEs of the bakery sector of the district of Chorrillos, using a type of correlational descriptive research, of non-experimental design and applying a survey to 138 microentrepreneurs of the bakery sector reaches the following conclusions: the Balanced Scorecard, as an innovative tool that summons all employees to meet the objective of the company and go after the fulfillment of the mission and vision is related to the business management of the MSEs and positively influences, the measurement of performance, as a management tool that facilitates the possibility of recognizing the development of progress and realizing if the company is well on track to realize its objectives, is related to business management of MSEs and positively influences, Continuous improvement and the application of a strategic map is related to the business management of MSEs and positively influence them, finally recommends that managers access courses and / or training that are useful for the best performance of their functions within the companies they direct.

Huaraca Molina(15), in his thesis proposes as a general objective to determine the relationship of the Balanced Scorecard with the Financial Statements of SMEs companies in the commercial sector and as specific objectives to recognize the link that exists between the Balanced Scorecard and the income statement, as well as to identify the relationship of the perspectives of the Balanced Scorecard with the state of financial situation of the SMEs of the commerce sector, line of sale of beauty products of the district of Lima period 2017. This work is a correlational research of non-experimental design - transversal and correlational - non-experimental, of quantitative method, the population is made up of 257 people, among them, the owners, administrators, managers and accountants of the SMEs, likewise, survey techniques and questionnaire tools with 20 questions were used, finally their research is concluded stating the following: 57,59 % of respondents have only completed secondary school, so they are unaware of financial, economic and administrative issues, which leads them only to receive day-to-day profits, 57,75 % of respondents almost always do not perform an adequate study of the cost of the product before being acquired for sale, so it is evident that they do not know the importance of the correct calculation of costs to determine its usefulness, 59,14 % of the SMEs under study manage a control of accounts payable guided by the policies of the company, this being alarming given that there is no analysis to know if it has liquidity or not to be able to face its current liabilities, causing that in some opportunities they become insolvent.

Gamarra Falcon(16), in his undergraduate thesis establishes as its main objective to determine the relationship between strategic planning and business development in the company Teleatento del Perú S.A.C, Callao, year 2017, and as specific objectives, determine the relationship between the Balanced Scorecard and business development, and determine the relationship of the administrative process with the business development of the company Teleatento del Perú S.A.C, Callao, year 2017 for which I use an applied research of non-experimental – cross-sectional design, with a level of correlational descriptive study, had a population of 200 collaborators and a sample of 132 collaborators, the information was collected using the survey technique and as an instrument the questionnaire consisting of 21 questions under the Likert scale was used, the following results were obtained: it was possible to demonstrate the relationship between the study variables, obtaining a relationship index of 0,693 demonstrating a positive correlation, on the other hand regarding the specific objectives demonstrated the relationship between the Balanced Scorecard and business development with a ratio index of 0,644 demonstrating a moderate positive correlation, a ratio index of 0,597 was also obtained, which demonstrates a moderate positive correlation between the administrative process and business development.

Alarcón Aburto(17), in his undergraduate thesis proposes as a general objective to determine the influence of strategic planning and business development of the MSMES of Ciudad de Dios – SJM, 2018 and as specific objectives: determine the influence of the organizational mission, organizational vision and organizational objectives with the business development of the MSEs of Ciudad de Dios – SJM, 2018, using an applied research design, non-experimental cross-section, explanatory or causal level, with a population made up of the 60 owners of the marketing MSEs of Ciudad de Dios, in this research no sample calculation was made, for being a census investigation; the survey was used as a research technique and as a data collection instrument to the questionnaire containing 20 questions, having as results according to the hypothesis test and analysis of the results table in the Pearson correlation statistic and the linear regression test, the rejection of the null hypothesis and the acceptance of the alternative hypothesis, Therefore, there was a very strong positive correlation of 0,932, concluding that there is a relationship between the study variables. Therefore, strategic planning is contributing 96,9 % to the business development of MSEs. On the other hand, there is a correlation of 0,990, 0,923 and 0,993 with a significance level less than 0,05 indicating that, if there is a significant influence between the mission, vision and organizational objectives with business development, respectively.

All these research works are a great contribution to substantiate the objective embodied in this thesis, since the analysis made to the importance of the Balanced Scorecard as a factor of development and growth for the various entrepreneurs, in different sectors the great influence of the Balanced Scorecard and its indicators is obtained as a result.

Theoretical bases

Balanced Scorecard

The creators of the Balanced Scorecard are the distinguished ones, Kaplan and Norton and has its origin when a study sponsored by the Nolan Norton Institute was developed, which was based on research to evaluate the results of companies since the ways of evaluating the performance of companies in the market were essentially based on financial indicators, and these did not offer complete information, and they were worthless. Kaplan and Norton said that results were obtained in the short term thanks to the financial indicators of that time, however, although companies believed that profits were obtained in the short term, they had less possibility to grow in the future. Both researchers and participants began to realize that the most promising way to measure company performance was a long-term multidimensional approach that included issues of productivity, quality, learning important to the company, and at that time all this was taken of little importance.(18)

Balanced Scorecard concepts

Sánchez Martorelli(19) argues that the Balanced Scorecard has taken several names. Some use the original English name; others use the transcription "Balanced Scorecard." Names such as "Balanced Scoreboard" and "Balanced System of Indicators" have also been disseminated.

Amo Baraybar(20) defines the Balanced Scorecard as a management method or technique that allows companies to translate their strategy into measurable and interrelated performance goals, thus facilitating the retention of key people in the organization and its resources.

Also, Villa Garnacha(21) points out that the BSC is a method of evaluating the performance of a company against the vision and strategy since it allows managers to obtain an overview of the performance of the business, which makes it.

According to Apaza Meza(22) the BSC is "a model that helps microentrepreneurs translate strategies into operational goals, allows organizations to generate organizational results and aligns the strategic positions of those directly involved in the business.

On the other hand, Villa Garnacha(21) mentions that:

"The Balanced Scorecard is a new framework that allows companies to translate strategy into operational goals, these provide guidance on how to achieve consistent business results and behaviors by key people in the organization".

Kaplan & Norton(18), point out that the Balanced Scorecard is an administrative technique that beyond a tactical or operational measurement, helps quantify the activities of an organization based on its vision and strategy, providing the necessary tools to head to success.

For this research, the conceptualization of Kaplan & Norton(18) will be taken into account.

Balanced Scorecard dimensions

Financial perspective: Alveiro Montoya(23) indicates that this perspective reflects the company's ability to capitalize on its achievements and convert them into profits, thus satisfying the needs of shareholders.

Amo Baraybar(20) states that: "The financial perspective, also called value, collects the needs of satisfying the shareholders of the organization, serving as a focus for the objectives and indicators of the rest of the perspectives.". Rodríguez Gutiérrez et al.(24) point out that the financial perspective aims to increase profitability. This perspective is particularly focused on the creation of shareholder value, with high rates of return, guarantee of growth and maintenance of the business. Finally, Kaplan & Norton(18) points out that this perspective is important to focus the other perspectives in the same line, it is the last to be fulfilled (since it is planned in the long term) but the first to be considered. Financial indicators compile economic information about the company driven by actions already taken and use that information to know how to proceed in the next period and know if there is improvement in the expected results or not. For this research, the conceptualization of Rodríguez Gutiérrez et al.(24) will be taken into account.

Customer and market perspective: Kaplan & Norton(18) indicates that this perspective establishes its objectives based on customer satisfaction, so it identifies the peculiarities of the market to which it is directed and plans its offer of products or services according to customer preferences. This perspective is designed to retain customers and increase their profitability. Quintero Beltrán & Osorio Morales(25) argues that this perspective is also recognized as a commercial perspective and refers to how it is intended to satisfy and retain customers so that they become loyal to the company or what strategies to establish to increase the number of customers. For Rampersad(26) this perspective deals with an external vision, in which it is desirable to measure customer satisfaction to maintain close relationships, understand their needs to satisfy and create relationships that are maintained over time, likewise, points out that at this point it would be appropriate to ask how customers relate to the company and what that means for them.

Internal Process Perspective: In this regard, Kaplan & Norton(18) states that this perspective is essentially a study of the internal processes of a company. This study usually includes the identification of resources and capabilities that the company itself needs to improve. The relationship between internal company processes and other collaborative processes is getting closer and answers the question: What should we consider in terms of customers and internal processes? Alveiro Montoya(23) describes that this indicator is linked to an excellently integrated and specific internal vision for each part of the organization, because it is more important to have an orientation for critical internal activities that achieve customer satisfaction. Emphasis should also be placed on the organization's key competencies, as well as the technologies required to achieve market leadership. In the opinion of Quintero Beltrán & Osorio Morales(25) the perspective of the internal process deals with the strategy in the internal processes of the company, the organizational structure and the creation of customer management, innovation, and social environments.

Learning and development perspective: The authors argue that this perspective is crucial for the development of the other perspectives, therefore it is used first. While other perspectives develop goals that define what an organization should focus on to excel, the learning and growth perspective focuses on the company's intangible assets and developing the key elements needed to help achieve goals. This perspective focuses on the importance of investing in improving the company's infrastructure, starting with the capabilities of employees, the capabilities of IT systems and employee motivation and empowerment. In addition, the coherence of the proposed objectives is taken into account, to have a clear understanding of them and thus an adequate development. Kaplan & Norton(18). In relation to this perspective, Alveiro Montoya(23) explains that this perspective is designed so that the organization includes values and forms of measurement, the capacity for improvement over time, because that is the only formula that can guarantee success. So that the company can achieve both efficiency and transparency in its work and achieve both innovation and added value in a tangible way. According to Quintero Beltrán & Osorio Morales(25) in this perspective, the competencies that the company must improve are considered, especially in human resources, which can generate motivation, training and other strategies.

Benefits of the Balanced Scorecard

Villa Garnacha(21) mentions that the main benefits of the Balanced Scorecard are: the alignment of the vision of the company with the employees, the restructuring of the strategy, the interpretation of the vision of the company, the unification of information from different areas and the communication of the objectives of the company to all employees. In turn, the director of a bank that implemented a balanced scorecard described the following benefits: turning vision and strategy into action, helping the organization focus on what needs to be done to create future value, being an integrated mechanism, useful as an agent of change.

Advantages of the Balanced Scorecard

Ahn(27) manifests seven advantages of the Balanced Scorecard:

Turning vision into measurable goals: Turning an organization's vision into precise actions that can be developed and measured is one of the key functions of the BSC methodology, so for each strategy it provides metrics that will be used to track the organization's goals. Detect errors and help correct them.

Alignment of the entire strategy: All elements of the strategic planning process align with the BSC. The objectives are aligned to the strategic initiatives, in the same way that these are aligned to the indicators, that is, the entire organization is correctly concentrated and directed towards the same objective. By implementing a strategy map, an organization's strategy can be organized into a cause-and-effect relationship.

Improve communication between members of the organization: Creating a strategy map is beneficial from a quantifiable point of view, making it an ideal complement to the implementation of a BSC, as it provides a holistic view of an organization's overall strategy, allowing each member to communicate more effectively about achieving goals based on their progress.

Stimulation of strategic transformations: The BSC methodology promotes and strengthens learning, usually when an error is detected in an organization, because it is immediately corrected, however, the reasons for the failure are not usually investigated. With the BSC, the overall functioning of the organization is optimized.

Give structure to your strategy: BSC helps organizational leaders ensure that all areas of the company keep their goals at the center, using specific metrics to implement their processes and track their actions.

Always maintain your strategy: If the strategy is organized, with the application of the BSC it is essential to carry out its constant review, this guarantees compliance in the execution of the same.

Better information management: With BSC, the correct performance indicators can be designed for each strategic objective, thus ensuring that each area is measured within the organization.

Organizations implementing BSC have been shown to have high-quality information management processes that lead to better decision making.

Basic components of the Balanced Scorecard

For Tello(28) the BSC is:

"The expression of a strategy pursued within a coherent framework through well-connected business objectives, measured by performance indicators dependent on the outcome of the specific objectives and supported by a set of projects that make up the organization. Therefore, the following are defined as the main components of the BSC: a series of causal relationships that express hypotheses about the strategies that will achieve the objectives set and their adequate support through performance indicators, a link of financial results with learning and growth perspectives, internal, financial and customer processes; Results should translate into quantified financial achievements, a balance of outcome indicators, measurements should create and stimulate organizational change, align projects with strategy prioritizing objectives."

Business development

Business Development Concepts

González Diaz(29) expresses the following: "business development represents the set of actions for the change of a company that aims to grow and improve its performance, either by increasing its presence in the market or its competitiveness".

Likewise, Jungbluth Voysest & Díaz Garay(30) states that it can be understood as the level of progress, optimization or improvement of the economy, effectiveness, efficiency, continuous improvement, and competitiveness that companies must have.

Rodriguez Diaz(31) defines business development as: "the process of evolution that a company or organization undergoes over time".

Dimensions of enterprise development

Economic profitability: Aguirre Ormaechea et al.(32) argue that: economic profitability is a margin calculation that measures the productivity of sales when making a profit, thus measuring the efficiency with which a firm manages its net investments. Tamayo(33) states that profitability is an external variable, since it affects the financial combination, the union of debt and equity destined for financing. On the other hand, Sánchez Flores(34) indicates that economic profitability is a measure, related to the efficiency with which the assets of a company are used during a given period, regardless of its financial source, that is, it is considered as a measure of the value creation capacity of the company's assets, regardless of how they are financed.

Product quality: Gómez Niño(35) states that quality is understood as the ideal, the optimal to meet the needs and create a new sense of satisfaction to consumers, which drives buyers to a particular product and not to another that has similar characteristics. In this regard, Ishikawa et al.(36) define that: quality is developing, designing, manufacturing, and maintaining a quality product that is the most economical, useful and always satisfactory for the consumer. On the other hand, Sánchez Carlessi et al.(37) states that: Quality ranges from product design to after-sales, through all internal processes where greater importance is given to both the external and internal customer.

Resource optimization: González Basabe et al.(38) argue that: "resource optimization can be defined as the best way to do business, because when we talk about resource optimization, we do not only refer to the ability to retain or eliminate some desirable aspect from the business point of view." Ramirez Borda(39) indicates that resource optimization implies the efficient management of resources, which can be tangible or intangible. Depending on the context, people, money, technology, and even time can be considered manageable resources.

Innovation: Schumpter(40) states that: innovation is the introduction of a new product or process that could be the point of difference, as well as opening a new market or the discovery of a new source of raw materials or intermediate products. Pavón Morote & Hidalgo Nuchera(41) argues that: innovation is the set of actions at a given time and place that lead to the successful introduction of an idea into the market for the first time in the form of a new product, service or method of organization and management. Suarez Mella(42) states that: innovation is nothing more than the process of developing something new or unknown based on the methodical study of the needs of an individual, group or organization to achieve an economic goal.

Prospects for enterprise development

Blázquez Santana et al.(43) propose the following perspectives:

Life cycle p.: From the point of view of this perspective, the company develops in phases, where each of them is the result of the previous one, creating a gradual growth with growth stages stopped by fluctuating difficulties. As a result, the company moves on to the next stage of growth. The logic behind this intermittent growth model is that, at each stage of growth, the company must adopt a specific profile defined by the relationship between size, age, strategy, organizational structure, and environment.

P. resource-based: This perspective focuses on the fact that the existence of surplus resources can be used in new areas, as an engine for decision-making about the growth and development of the company, in which it certainly plays a fundamental role in the entrepreneurial attitude of an entrepreneur or manager.

P. based on motivation.: This perspective helps to understand why some entrepreneurs act in a certain way in certain decisions, especially in terms of business growth; while others, with the same or even greater resources, do not develop a more entrepreneurial attitude.

Characteristics of business development

According to Mejias(44) indicates that there are several aspects that coexist with business development, such as:

· Constant training, to promote productivity.

· Business culture, which includes the goals and values of the company and each one that conforms them.

· Leadership, someone who possesses the indispensable skills to drive production and empathize with the team.

· Innovation, where knowledge management allows the company to adapt to an increasingly globalized market.

Elements of enterprise development

On the other hand, Delfín Pozos & Acosta Márquez(45) indicates that business development: "is structured with various elements with which each entrepreneur can lead an organization to achieve its objectives, these being: economic growth, business culture, leadership and knowledge management and innovation".

MSMEs: "The Micro and Small Enterprise is the economic unit constituted by a natural or legal person, under any form of organization or business management contemplated in the current legislation, which aims to develop activities of extraction, transformation, production, commercialization of goods or provision of services." Congreso de la República.(46) It should be mentioned that this legislation only conceptualizes micro and small enterprises, generating a vacuum with respect to medium and large companies, Congreso de la República(47) mentions the criterion that characterizes the annual sales margin for small and medium enterprises, as shown in the following table.

Strategic planning: Sallenave(48) argues that: "Strategic planning is the process by which leaders define their objectives and actions over time. In fact, the concept of strategy and planning are intimately linked, since both designate a sequence of actions ordered in time, in such a way that one or more objectives can be achieved".

Strategic objectives: Andía Valencia(49) argues that they must be: measurable, quantifiable, achievable, understandable, and motivating since they are the most relevant and important results that the organization intends to achieve to fulfill its mission.

Management indicators: Sánchez Rodríguez(50) states that they are: "the integral processes that facilitate the measurement of the achievements and the fulfillment of the mission and objectives of the organization in its different areas".

METHODOLOGY

Cortés Cortés & Iglesias León(51) argues that: "Methodology is the science that teaches us to direct a certain process efficiently and effectively to achieve the desired results and aims to give us the strategy to follow in the process."

Research method

For this research, the scientific method was used as a general method, since a problem was found, it was observed, possible solutions were conjectured through hypotheses, and finally the hypotheses were corroborated.

In this regard Tamayo(33) he points out that "The scientific method is a set of procedures by which scientific problems are raised and the hypothesis and instruments of research work are tested."

Research approach

This study uses a quantitative approach, since it validates the hypothesis and measures variables using non-probabilistic statistics to study the information obtained from the applied surveys.

In relation to the afore mentioned Cortés Cortés & Iglesias León(51), they maintain that the quantitative approach uses numerical measurements, data collection and analyzes them to answer the research questions, verify hypotheses by measuring parameters, collect frequencies and statistics on the population being studied.

Type of research

This research is applied because it aims to specify the relationship of the study variables and these with their dimensions based on existing studies.

Using the words of Martínez de Sánchez(52) indicates that applied research uses the knowledge that has already been acquired in basic research, however, it not only does so to existing knowledge, but also seeks new, but increasingly specific.

Research design

The design of this research is non-experimental cross-sectional.

Non-experimental. -According to Cortés Cortés & Iglesias León(51) states that: "non-experimental research is one that does not deliberately manipulate the variables to be studied. What this type of research does is to observe phenomena as they occur in their current context, and then analyze it."

Transverse. - In the opinion of Hernández et al.(53) "cross-sectional designs or also known as transactional collect data at a single moment and in a single time, their objective is to describe variables and analyze their incidence or interrelation at a given time."

Level of research

The present research is of descriptive level - causal correlational because it seeks to know the relationship or degree of association that exists between the variables Balanced Scorecard and business development.

Descriptive. - Hernández et al.(53) states that this type of research allows to establish a description of a particular form of a certain phenomenon, some element or situation where the objective is to know more about the customs, understand the habit and the location that stands out through the explanation of the work, elements and their individuals.

Correlational - causal. – Ñaupas Paitán et al.(54) mentions that "it is a design of a more complex investigation because it tries to explain the causes and factors of a problem, that is, it will look for one or two main causes two or more secondary causes, called factors. It is used when you want to determine the degree of influence of an independent variable on the dependent variable, in a comparative way."

Population

Arias Odón(55) states that "it is a finite or infinite set of elements with common characteristics for which the conclusions of the research will be extensive".

For this research, the selected population are the different MSMEs specifically the commercial sector (purchase-sale, without alteration), which are registered in the District Municipality of San Vicente, which amount to 68 according to the census provided by the Provincial Municipality of Cañete on August 27, 2019.

Selected sample

For the development of the present research, intentional non-probability sampling was applied with a total of 68 respondents.

In this regard Arias Odón(55) states that "intentional or office sampling, since the elements are chosen based on criteria or judgments pre-established by the researcher."

On the other hand, Naghi Namakforoosh(56) argues that "If the population under study is small, all its members should be studied, but if it is large, it is convenient to choose a representative sample".

Technique

Survey

For López Roldán & Fachelli(57) it is: "in the first instance a technique of data collection through the investigation of the subjects whose objective is to obtain systematic concepts of the research problem".

Instrument

Questionnaire

García Cordova(58) argues that: "it is a system of rational questions, ordered in a coherent way, both logically and psychologically, expressed in a simple and understandable language".

Data processing and analysis

Microsoft Excel was used as a basic tool for data processing, showing an exhaustive analysis through illustrations such as: tables and graphs.

Descriptive statistics will be used, and the database will be subjected to statistical analysis in the SPSS program, for the contracting of the hypothesis Spearman's Rho statistician was used, and for the validation of the instrument Cronbach's Alpha.

Therefore, because inferential measurement techniques may choose to determine the relationship between factors, to know if there is a positive or negative correlation, a nonparametric Spearman correlation range test will be performed to find the correlation between the two quantitative variables Calderón Ortiz et al.(59).

Dependence is analyzed because the information responds to a normal curve, and SPSS data programming is used to compare it with parameter factors to determine significance level according to Kolmogorov's normality test 29 Finch Stoner et al.(60).

RESULTS

Independent variable Balanced Scorecard

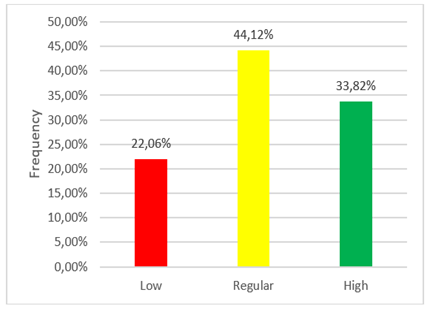

According to table N°1 and figure N°1, it is taken with respect to the independent variable Balanced Scorecard that 22,06 % (n=15) have a low level, 44,12 % (n=30) a regular level and 33,82 % (n=23) a high level.

|

Table 1. Independent variable: Balanced Scorecard |

|||

|

|

Frequency |

Percentage |

|

|

|

Low |

15 |

22,06 |

|

Regular |

30 |

4,12 |

|

|

High |

23 |

33,82 |

|

|

Total |

68 |

100,0 |

|

Figure 1. Independent variable: Balanced Scorecard

Financial perspective dimension

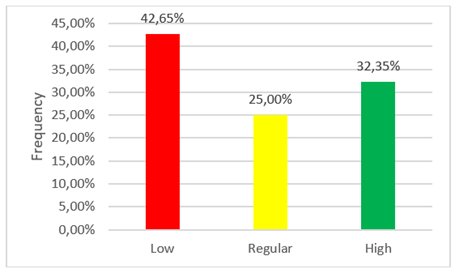

According to table N°2 and figure N°2, it is taken with respect to the financial perspective dimension of the independent variable Balanced Scorecard that 42,65 % (n=29) have a low level, 25,00 % (n=17) a regular level and 32,35 % (n=22) a high level.

|

Table 2. Dimension: financial perspective |

||

|

|

Frequency |

Percentage |

|

Low |

29 |

42,65 |

|

Regular |

17 |

25,00 |

|

High |

22 |

32,35 |

|

Total |

68 |

100,0 |

Figure 2. Dimension: financial perspective

Customer perspective dimension

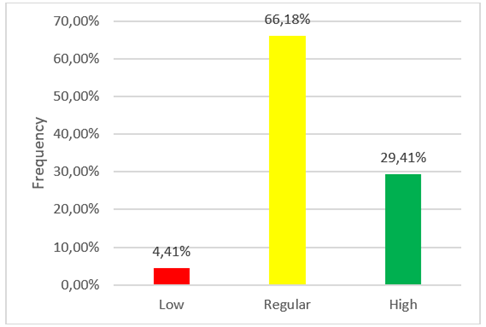

According to table N°3 and figure N°3, it is taken with respect to the client’s perspective dimension of the independent variable Balanced Scorecard that 4,41 % (n=3) have a low level, 66,18 % (n=45) a regular level and 29,41 % (n=20) a high level.

|

Table 3. Dimension: customer perspective |

||

|

|

Frequency |

Percentage |

|

Low |

3 |

4,41 |

|

Regular |

45 |

66,18 |

|

High |

20 |

29,41 |

|

Total |

68 |

100,0 |

Figure 3. Dimension: customer perspective

Process perspective dimension

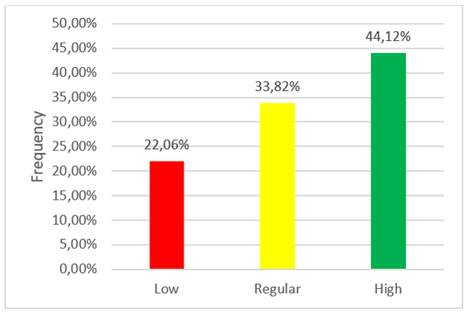

According to table N°4 and figure N°4, it is taken with respect to the process perspective dimension of the independent variable Balanced Scorecard that 22,06 % (n=15) have a low level, 33,82 % (n=23) a regular level and 44,12 % (n=30) a high level.

|

Table 4. Dimension: process perspective |

|||

|

|

Frequency |

Percentage |

|

|

|

Low |

15 |

22,06 |

|

Regular |

23 |

33,82 |

|

|

High |

30 |

44,12 |

|

|

Total |

68 |

100,0 |

|

Figure 4. Dimension: process perspective

Dimension Perspective of formation and growth

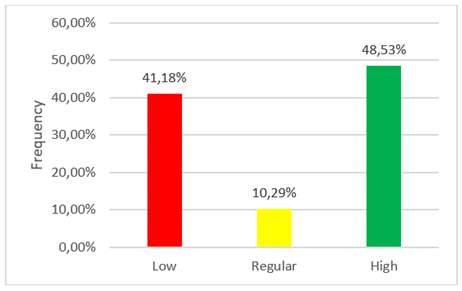

According to table N°5 and figure N°5, it is taken with respect to the formation and growth dimension of the independent variable Balanced Scorecard that 41,18 % (n=28) have a low level, 10,29 % (n=7) a regular level and 48,53 % (n=33) a high level

|

Table 5. Perspective of formation and growth |

|||

|

|

Frequency |

Percentage |

|

|

|

Low |

28 |

41,18 |

|

Regular |

7 |

10,29 |

|

|

High |

33 |

48,53 |

|

|

Total |

68 |

100,0 |

|

Figure 5. Dimension: Perspective of formation and growth

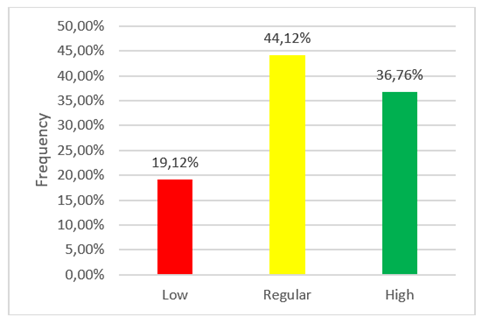

Dependent variable business development

According to table N°6 and figure N°6, it is taken with respect to the dependent variable business development that 19,12 % (n=13) present a low level, 44,12 % (n=30) a regular level and 36,76 % (n=25) a high level.

|

Table 6. Dependent variable: business development |

|||

|

|

Frequency |

Percentage |

|

|

|

Low |

13 |

19,12 |

|

Regular |

30 |

44,12 |

|

|

High |

25 |

36,76 |

|

|

Total |

68 |

100,0 |

|

Figure 6. Dependent variable: business development

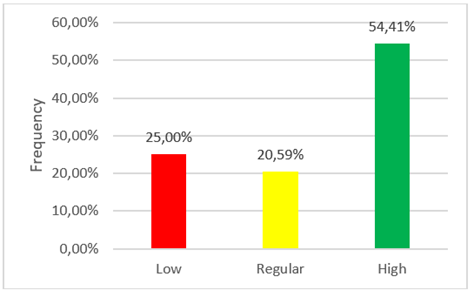

Economic profitability dimension

According to table N°7 and figure N°7, it is taken with respect to the economic profitability dimension of the dependent variable business development that 25,00 % (n=17) present a low level, 20,59 % (n=14) a regular level and 54,41 % (n=37) a high level.

|

Table 7. Dimension: economic profitability |

|||

|

|

Frequency |

Percentage |

|

|

|

Low |

17 |

25,00 |

|

Regular |

14 |

20,59 |

|

|

High |

37 |

54,41 |

|

|

Total |

68 |

100,0 |

|

Figure 7. Dimension: economic profitability

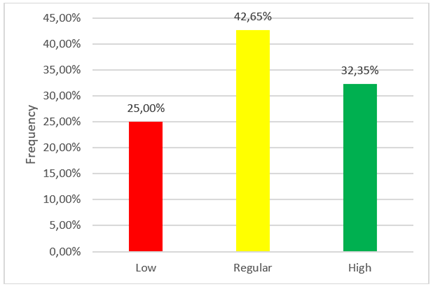

Product quality dimension

According to table N° 8 and figure N°8, with respect to the product quality dimension of the dependent variable business development, 25,00 % (n=17) have a low level, 42,65 % (n=29) a regular level and 32,35 % (n=22) a high level.

|

Table 8. Dimension: product quality |

|||

|

|

Frequency |

Percentage |

|

|

|

Low |

17 |

25,00 |

|

Regular |

29 |

42,65 |

|

|

High |

22 |

32,35 |

|

|

Total |

68 |

100,0 |

|

Figure 8. Dimension: product quality

Product optimization dimension

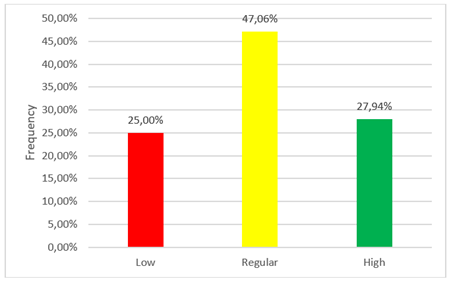

According to table No. 9 and figure No. 9, it is taken with respect to the product optimization dimension of the dependent variable business development that 25,00 % (n = 17) have a low level, 47,06 % (n = 32) a regular level and 27,94 % (n = 19) a high level.

|

Table 9. Dimension: Product Optimization |

|||

|

|

Frequency |

Percentage |

|

|

|

Low |

17 |

25,00 |

|

Regular |

32 |

47,06 |

|

|

High |

19 |

27,94 |

|

|

Total |

68 |

100,0 |

|

Figure 9. Dimension: Product Optimization

Innovation dimension

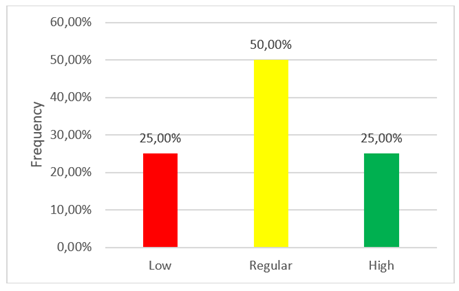

According to table N° 10 and figure N°10, we have with respect to the innovation dimension of the dependent variable business development that 25 % (n=17) have a low level, 50 % (n=34) a regular level and 25 % (n=17) a high level.

|

Table 10. Dimension: innovation |

||

|

|

Frequency |

Percentage |

|

Low |

17 |

25,00 |

|

Regular |

34 |

50,00 |

|

High |

17 |

25,00 |

|

Total |

68 |

100,0 |

Figure 10. Dimension: innovation

Hypothesis testing

General hypothesis

H0: The Balanced Scorecard does not significantly influence the business development of MSMEs in the province of Cañete, 2021.

H1: The Balanced Scorecard significantly influences the business development of MSMEs in the province of Cañete, 2021.

|

Table 11. Fit test of the models and R2 coefficient of the variable Balanced Scorecard and Business Development |

||||||

|

Model |

Likelihood logarithm -2 |

Chi2 |

Gl |

Gis. |

|

|

|

Intersection only Final |

120,690 5,017 |

115,673 |

2 |

0,000 |

Cox and Snell |

0,818 |

|

Nagelkerke |

0,933 |

|||||

|

McFadden |

0,814 |

|||||

In table No. 11 according to the results analyzed, it is indicated that the value of Nagelkerke's R 2 coefficient is 0,933, which explains that the Balanced Scorecard variable produces a variation of 93,3 % in the business development variable, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, indicating that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the business development of MSMEs in the province of Cañete, 2021.

Specific hypothesis

Specific hypothesis 1

H0: The Balanced Scorecard does not significantly influence the economic profitability of MSMEs in the province of Cañete, 2021.

H1: The Balanced Scorecard significantly influences the economic profitability of MSMEs in the province of Cañete, 2021.

|

Table 12. Fit test of the models and R2 coefficient of Balanced Scorecard and Economic Profitability |

||||||

|

Model |

Likelihood logarithm - 2 |

Chi2 |

Gl |

Gis. |

|

|

|

Intersection only Final |

74,511 9,947 |

64,564 |

2 |

0,000 |

Cox and Snell |

0,613 |

|

Nagelkerke |

0,708 |

|||||

|

McFadden |

0,473 |

|||||

In table No. 12 according to the results analyzed, it is indicated that the value of Nagelkerke's R 2 coefficient is 0,708, which explains that the Balanced Scorecard variable produces a variation of 70,8 % in the economic profitability dimension of the business development variable, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, indicating that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the economic profitability of MSMEs in the province of Cañete, 2021.

Specific hypothesis 2

H0: The Balanced Scorecard does not significantly influence the product quality of MSMEs in the province of Cañete, 2021.

H1: The Balanced Scorecard significantly influences the product quality of MSMEs in the province of Cañete, 2021.

|

Table 13. Fit test of the models and R2 coefficient of Balanced Scorecard and Product Quality |

||||||

|

Model |

Likelihood logarithm-2 |

Chi2 |

Gl |

Gis. |

|

|

|

Intersection only Final |

66,957 13,319 |

53,638 |

2 |

0,000 |

Cox and Snell |

0,546 |

|

Nagelkerke |

0,618 |

|||||

|

McFadden |

0,367 |

|||||

In table No. 13 according to the results analyzed, it is indicated that the value of Nagelkerke’s R 2 coefficient is 0,618, which explains that the Balanced Scorecard variable produces a variation of 61,8 % in the product quality dimension of the business development variable, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, indicating that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the product quality of MSMEs in the province of Cañete, 2021.

Specific hypothesis 3

H0: The Balanced Scorecard does not significantly influence the optimization of resources of MSMEs in the province of Cañete, 2021.

H1: The Balanced Scorecard significantly influences the optimization of resources of MSMEs in the province of Cañete, 2021.

|

Table 14. Fit test of the models and R2 coefficient of Balanced Scorecard and Resource Optimization |

||||||

|

Model |

Likelihood logarithm - 2 |

Chi2 |

Gl |

Gis. |

|

|

|

Intersection only Final |

61,489 13,929 |

47,561 |

2 |

0,000 |

Cox and Snell |

0,503 |

|

Nagelkerke |

0,572 |

|||||

|

McFadden |

0,331 |

|||||

In table No. 14 according to the results analyzed, it is indicated that the value of Nagelkerke's R 2 coefficient is 0,572, which explains that the Balanced Scorecard variable produces a variation of 57,2 % in the resource optimization dimension of the business development variable, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, indicating that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the optimization of resources of MSMEs in the province of Cañete, 2021.

Specific hypothesis 4

H0: The Balanced Scorecard does not significantly influence the innovation of MSMEs in the province of Cañete, 2021.

H1: The Balanced Scorecard significantly influences the innovation of MSMEs in the province of Cañete, 2021.

|

Table 15. Fit test of the models and R2 coefficient of Balanced Scorecard and Innovation |

||||||

|

|

Likelihood logarithm - 2 |

Chi2 |

Gl |

Gis. |

|

|

|

|

71,330 9,699 |

61,631 |

2 |

0,000 |

Cox and Snell |

0,596 |

|

Nagelkerke |

0,681 |

|||||

|

McFadden |

0,436 |

|||||

In table No. 15 according to the results analyzed, it is indicated that the value of Nagelkerke's R 2 coefficient is 0,681, which explains that the Balanced Scorecard variable produces a variation of 68,1 % in the innovation dimension of the business development variable, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, indicating that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the innovation of MSMEs in the province of Cañete, 2021.

DISCUSSION

Based on what is stated in the general objective: to determine, what is the influence of the Balanced Scorecard on the business development of MSMEs in the province of Cañete 2021, the research has obtained as a result that in the independent variable Balanced Scorecard 22,06 % (n = 15) have a low level, 44,12 % (n = 30) a regular level and 33,82 % (n = 23) a high level; In addition, regarding the dependent variable Business Development, 19,12 % (n=13) had a low level, 44,12 % (n=30) a regular level and 36,76 % (n=25) a high level; It was also had that the value of Nagelkerke's R 2 coefficient is 0,933, which explains that the Balanced Scorecard variable produces a variation of 93,3 % in the business development variable, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, which indicates that it is statistically significant. so the Balanced Scorecard significantly influences the business development of MSMEs in the province of Cañete, 2021, these results were contrasted with the research of Colareta Arriola(14) in his bachelor's thesis called: The Balanced Scorecard and business management in the MSEs of the bakery sector of the district of Chorrillos 2017, where he indicates that the statistical results obtained allow us to affirm the general hypothesis, the Balanced Scorecard is related to the business management of the MSEs of the bakery sector of Chorrillos; this statement is based on the data obtained where X 2 tabular (31,41) is lower than the X 2 obtained (160,16), so it is understood that the Balanced Scorecard positively influences the business management of the MSMEs of the bakery sector of Chorrillos.

Based on what is stated in specific objective 1: to determine if the Balanced Scorecard influences the economic profitability of MSMEs in the province of Cañete 2021, the research has obtained as a result that in the independent variable Balanced Scorecard 22,06 % (n = 15) have a low level, 44,12 % (n = 30) a regular level and 33,82 % (n = 23) a high level; In addition, regarding the economic profitability dimension of the dependent variable business development, it was necessary that 25,00 % (n = 17) have a low level, 20,59 % (n = 14) a regular level and 54,41 % (n = 37) a high level, we also had the value of Nagelkerke's R 2 coefficient is 0,708 which explains that the Balanced Scorecard variable produces a variation of 70,8 % in the economic profitability dimension of the development variable business, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, which indicates that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the economic profitability of MSMEs in the province of Cañete, 2021; these results were verified with the research of Huaraca Molina(15) in his bachelor's thesis called: "Balanced Scorecard and the financial statements of SMEs in the commerce sector, turn of sale of beauty products, district of Lima period 2017 ", where it concludes that there is a relationship between the Balanced Scorecard and the Financial Statements of the SMEs of the commerce sector since the tasks to be executed are assembled and share a relationship.

Based on what is stated in specific objective 2: To determine if the Balanced Scorecard influences the quality of the product of MSMEs in the province of Cañete 2021, the research has obtained as a result that in the independent variable Balanced Scorecard 22,06 % (n = 15) have a low level, 44,12 % (n = 30) a regular level and 33,82 % (n = 23) a high level; In addition, regarding the product quality dimension of the dependent variable Business Development, it was obtained that 25,00 % (n=17) have a low level, 42,65 % (n=29) a regular level and 32,35 % (n=22) a high level, we also had the Nagelkerke R 2 coefficient value is 0,618, which explains that the Balanced Scorecard variable produces a variation of 61,8 % in the product quality dimension of the variable business development, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, which indicates that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the quality of the product of MSMEs in the province of Cañete, 2021, these results were verified with the research of Mendez & Mendez(10) in its scientific article entitled: "The Balanced Scorecard and its effect on the performance of organizations", whose final conclusion is that this tool has a guaranteed effect on the performance of organizations thanks to its adaptability and flexibility because it allows constant monitoring on the implementation of planned strategies, this places the BSC as the best tool to improve organizational performance in all aspects.

Based on what is stated in specific objective 3: Determine if the Balanced Scorecard influences the optimization of resources of MSMEs in the province of Cañete 2021, the research has obtained as a result that in the independent variable Balanced Scorecard 22,06 % (n = 15) have a low level, 44,12 % (n = 30) a regular level and 33,82 % (n = 23) a high level; In addition, regarding the dimension Resource optimization of the dependent variable Business Development it was obtained that 25,00 % (n = 17) have a low level, 47,06 % (n = 32) a regular level and 27,94 % (n = 19) a high level, we also had the value of Nagelkerke's R 2 coefficient is 0,572 which explains that the Balanced Scorecard variable produces a variation of 57,2 % in the resource optimization dimension of the variable business development, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, which indicates that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the optimization of resources of MSMEs in the province of Cañete, 2021, these results were verified with the research of Colimba Farinango (11) entitled: "Analysis of the application of the Balanced Scorecard in the company Inno Fiber CÍA. LTDA.", where he mentions that the BSC is not only an evaluation tool but also helps to achieve a better Focus and control of all administrative processes, through strategic objectives in order to have an optimal business development in the company, making it a system to obtain the triumph against the competition and have a better productivity that implies increasing the development of the company.

Based on what is stated in specific objective 4: To determine if the Balanced Scorecard influences the innovation of MSMEs in the province of Cañete 2021, the research has obtained as a result that in the independent variable Balanced Scorecard 22,06 % (n = 15) have a low level, 44,12 % (n = 30) a regular level and 33,82 % (n = 23) a high level; In addition, regarding the innovation dimension of the dependent variable Business Development, it was obtained that 25 % (n = 17) have a low level, 50 % (n = 34) a regular level and 25 % (n = 17) a high level; We also had the value of Nagelkerke's R 2 coefficient is 0,681, which explains that the Balanced Scorecard variable produces a variation of 68,1 % in the innovation dimension of the business development variable, stating that there is a significant dependence with p_valor=0,000 which is less than 0,05, which indicates that it is statistically significant. Therefore, the null hypothesis is rejected, this means: The Balanced Scorecard significantly influences the innovation of MSMEs in the province of Cañete, 2021, these results were verified with the research of Jiménez Silva et al.(12) entitled; "The management of organizational knowledge based on the perspectives of the Balanced Scorecard as a key factor for the innovation of SMEs", where he affirms that the perspectives of the BSC favors an appropriate management of intellectual capital to achieve business innovation and achieve competitive advantage.

CONCLUSIONS

· It was found that MSMEs in the province of Cañete have great support in the Balanced Scorecard since this tool helps them in business development.

· It was evidenced that the Balanced Scorecard significantly influences the economic profitability of MSMEs in the province of Cañete, which implies that the Balanced Scorecard is related to the economic profitability of MSMEs in the province of Cañete, a statement supported by the statistical data obtained.

· It was evidenced that the Balanced Scorecard significantly influences the quality of the product of the MSMEs of the province of Cañete, which implies that the Balanced Scorecard is related to the quality of the product of the MSMEs of the province of Cañete, a statement supported by the statistical data obtained.

· It was evidenced that Balanced Scorecard significantly influences the optimization of resources of MSMEs in the province of Cañete, which implies that the Balanced Scorecard is related to the optimization of resources of MSMEs in the province of Cañete, a statement based on the statistical data obtained.

· It is evident that the Balanced Scorecard significantly influences the innovation of MSMEs in the province of Cañete, which implies that the Balanced Scorecard is related to the innovation of MSMEs in the province of Cañete, an affirmation supported by the statistical data obtained.

REFERENCES

1. Bada Carbajal LM, Rivas Tovar LA. Tipologías y modelos de cadenas productivas en las Mipymes. Lebret [Internet]. 2009 [cited 2023 Sep 20];1(1):173–98. Available from: https://dialnet.unirioja.es/servlet/articulo?codigo=5983147&info=resumen&idioma=ENG

2. Valdés Díaz de Villegas JA, Sánchez Soto GA. LAS MIPYMES EN EL CONTEXTO MUNDIAL: SUS PARTICULARIDADES EN MÉXICO. Iberoforum Revista de Ciencias Sociales de la Universidad Iberoamericana [Internet]. 2012 [cited 2023 Sep 21];7(14):126–56. Available from: https://www.redalyc.org/articulo.oa?id=211026873005

3. Dini M, Stumpo G. Mipymes en América Latina: un frágil desempeño y nuevos desafíos para las políticas de fomento [Internet]. 1ra ed. Comisión Económica para América Latina y el Caribe (CEPAL). Vitacura - Santiago de Chile: Comisión Económica para América Latina y el Caribe; 2018 [cited 2023 Sep 11]. 1–491 p. Available from: https://www.cepal.org/es/publicaciones/44148-mipymes-america-latina-un-fragil-desempeno-nuevos-desafios-politicas-fomento

4. Mendoza Mieles JJ, Macías Macías GM, Parrales Poveda ML. Desarrollo empresarial de las mipymes ecuatorianas: su evolución 2015-2020. Revista Publicando [Internet]. 2021 Jan 9 [cited 2023 Sep 20];8(31):320–37. Available from: https://revistapublicando.org/revista/index.php/crv/article/view/2253

5. Álvarez Contreras DE, Jiménez Lyons KA. La consultoría y asesoría: aliada estratégica para el fortalecimiento empresarial de las MIPYMES en Colombia. Tendencias [Internet]. 2020 Jun 30 [cited 2023 Sep 11];21(1):252–71. Available from: https://revistas.udenar.edu.co/index.php/rtend/article/view/5608

6. Bravo García S, Masso Álzate JA, López Duque SY, Romero Palacios WE. Comparative study of micro, small and medium Companies in Colombia. Revista Venezolana De Gerencia [Internet]. 2022 [cited 2023 Sep 11];27(8):765–86. Available from: https://produccioncientificaluz.org/index.php/rvg/article/view/39179/43975

7. Instituto Nacional de Estadística e Informática. Perú: Estructura Empresarial, 2018 [Internet]. Lima - Perú; 2019 Nov [cited 2023 Sep 11]. Available from: https://www.inei.gob.pe/media/MenuRecursivo/publicaciones_digitales/Est/Lib1703/libro.pdf

8. Arasti Z, Zandi F, Bahmani N. Business failure factors in Iranian SMEs: Do successful and unsuccessful entrepreneurs have different viewpoints? Journal of Global Entrepreneurship Research [Internet]. 2014 Dec [cited 2023 Sep 21];4(1):1–14. Available from: https://www.researchgate.net/publication/284505303_Business_failure_factors_in_Iranian_SMEs_Do_successful_and_unsuccessful_entrepreneurs_have_different_viewpoints

9. Gutarra R, Valente A. The peruvian technological MSMEs to 2030. Strategies for their insertion to industrie 4.0. Nova scientia [Internet]. 2018 [cited 2023 Sep 11];10(20):754–78. Available from: https://dialnet.unirioja.es/servlet/articulo?codigo=6938611&info=resumen&idioma=ENG

10. Mendez JC., Mendez MA. El Balanced Scorecard y su efecto en el desempeño de las organizaciones. Revista Espacios [Internet]. 2021 Dec 15 [cited 2023 Sep 20];42(23):66–77. Available from: https://revistaespacios.com/a21v42n23/21422306.html

11. Colimba Farinango EJ. Análisis de la aplicación del balanced scorecard en la empresa Inno Fiber Cía. Ltda. [Internet]. [Ibarra - Ecuador]: Tesis de Licenciatura - Universidad Técnica del Norte; 2022 [cited 2023 Oct 9]. Available from: http://repositorio.utn.edu.ec/handle/123456789/13014

12. Jiménez Silva EE, Lema Cerda LA, Larrea Altamirano JF. La gestión del conocimiento organizacional basado en las perspectivas del Balanced Scorecard como factor clave para la innovación de las PYMES. Revista Publicando [Internet]. 2017 Oct 20 [cited 2023 Oct 9];4(12):640–57. Available from: https://revistapublicando.org/revista/index.php/crv/article/view/746

13. Delgado Requejo Y. Balanced Scorecard para la gestión empresarial de la empresa CACIDEP S.A.C., Cajamarca [Internet]. Repositorio Institucional - UCV. [Chiclayo - Perú]: Tesis de Maestría - Universidad César Vallejo; 2022 [cited 2023 Sep 11]. Available from: https://repositorio.ucv.edu.pe/handle/20.500.12692/78363

14. Colareta Arriola CR. El balanced scorecard y la gestión empresarial en las mypes del sector panadero del distrito de Chorrillos, 2017 [Internet]. Repositorio Institucional - UIGV. [Lima - Perú]: Tesis de Licenciatura - Universidad Inca Garcilaso de la Vega; 2018 [cited 2023 Sep 11]. Available from: http://repositorio.uigv.edu.pe/handle/20.500.11818/3527

15. Huaraca Molina JMV. Balanced Scorecard y los Estados Financieros de las Pymes del sector comercio, giro de venta de productos de belleza, distrito de Lima periodo 2017 [Internet]. Universidad César Vallejo. [Lima - Perú]: Tesis de Licenciatura - Universidad César Vallejo; 2018 [cited 2023 Sep 11]. Available from: https://repositorio.ucv.edu.pe/handle/20.500.12692/31467

16. Marcelo KVG, Claudio BAM, Ruiz JAZ. Impact of Work Motivation on service advisors of a public institution in North Lima. Southern Perspective / Perspectiva Austral 2023;1:11–11. https://doi.org/10.56294/pa202311.

17. David BGM, Ruiz ZRZ, Claudio BAM. Transportation management and distribution of goods in a transportation company in the department of Ancash. Southern Perspective / Perspectiva Austral 2023;1:4–4. https://doi.org/10.56294/pa20234.

18. Gamarra Falcon EM. Planificación Estratégica y su relación con el Desarrollo Empresarial en la empresa Teleatento del Perú SAC, Callao, año 2017 [Internet]. Universidad César Vallejo. [Lima - Perú]: Tesis de Licenciatura - Universidad César Vallejo; 2017 [cited 2023 Sep 11]. Available from: https://repositorio.ucv.edu.pe/handle/20.500.12692/12406

19. Alarcón Aburto AD. La planeación estratégica y su influencia en el desarrollo empresarial de las Mypes de Ciudad de Dios – SJM, 2018 [Internet]. Universidad César Vallejo. [Lima - Perú]: Tesis de Licenciatura - Universidad César Vallejo; 2018 [cited 2023 Sep 11]. Available from: https://repositorio.ucv.edu.pe/handle/20.500.12692/19383

20. Kaplan RS, Norton DP. The Balanced Scorecard: Translating Strategy Into Action [Internet]. Massachusetts - EEUU: Harvard Business Press; 2009 [cited 2023 Sep 11]. 1–322 p. Available from: https://books.google.com/books/about/The_Balanced_Scorecard.html?id=mRHC5kHXczEC

21. Sánchez Martorelli JR. Indicadores de gestión empresarial : De la estrategia a los resultados [Internet]. Indiana - EEUU: Palibrio; 2013 [cited 2023 Sep 20]. 1–172 p. Available from: https://books.google.com/books/about/Indicadores_de_Gestin_Empresarial.html?hl=es&id=Ic7RdmsTSu4C

22. Amo Baraybar F. El Cuadro de Mando Integral “Balanced Scorecard” [Internet]. 1ra ed. Madrid - España: ESIC Editorial; 2011 [cited 2023 Sep 11]. 1–81 p. Available from: https://books.google.com/books/about/El_Cuadro_de_Mando_Integral_Balanced_Sco.html?hl=es&id=zJkkDwAAQBAJ

23. Villa Garnacha ME. El cuadro de mando integral: concepto, enfoques y perspectivas. Formación y crecimiento directivo [Internet]. 2015 [cited 2023 Sep 21];8(1):173–85. Available from: https://repository.uamerica.edu.co/bitstream/20.500.11839/713/3/COL0104715-2015-1-FCD.pdf

24. Apaza Meza M. Balanced scorecard gerencia estratégica y del valor [Internet]. Lima - Perú: Instituto de Investigación El Pacífico; 2005 [cited 2023 Sep 11]. 1–703 p. Available from: https://catalogobiblioteca.ingemmet.gob.pe/cgi-bin/koha/opac-detail.pl?biblionumber=3467

25. Alveiro Montoya C. El balanced scorecard como herramienta de evaluación en la gestión administrativa. Revista Científica “Visión de Futuro” [Internet]. 2011 May 30 [cited 2023 Sep 11];15(2):1–26. Available from: https://www.redalyc.org/articulo.oa?id=357935478003

26. Rodríguez Gutiérrez R del C, Carpio Ortiz F, Obando Pereda M. Plan de Implementación Estratégica de una Vidriera Arequipeña Aplicando la Metodología del Balanced Scorecard. Sinergia e Innovación [Internet]. 2015 [cited 2023 Sep 20];3(2):123–36. Available from: https://repositorioacademico.upc.edu.pe/handle/10757/592895

27. Quintero Beltrán LC, Osorio Morales LM. Balanced Scorecard como herramienta para empresas en estado de crisis. Revista CEA [Internet]. 2018 Aug 30 [cited 2023 Sep 20];4(8):75–94. Available from: https://revistas.itm.edu.co/index.php/revista-cea/article/view/1049/1401

28. Malaver YYV, Claudio BAM, Ruiz JAZ. Quality of service and user satisfaction of a police station in a district of northern Lima. Southern Perspective / Perspectiva Austral 2024;2:20–20. https://doi.org/10.56294/pa202420.