doi: 10.56294/dm2024.630

ORIGINAL

Management and efficiency in highly complex public healthcare: an analysis of financial ratios and non-parametric statistic

Gestión y eficiencia en sanidad pública de alta complejidad: un análisis de ratios financieros y estadística no paramétrica

Robinson Dueñas Casallas1 ![]() *,

Cristina Crespo Soler2

*,

Cristina Crespo Soler2 ![]() *, Vicente Mateo Ripoll Feliu3

*, Vicente Mateo Ripoll Feliu3 ![]() *, Carlos Arturo Alvarez Moreno4

*, Carlos Arturo Alvarez Moreno4 ![]() *

*

1Faculty of Economic Sciences, New Granada Military University, member of AICOGestión, Bogotá, Colombia.

2PDI Holder D University, Vice Dean of Participation, Volunteering and Equality. Accounting Department, Faculty of Economics University of Valencia, member of AICOGestión, Spain.

3PDI Titular D University, Accounting Department–Faculty of Economics University of Valencia, President of the Ibero-American Association of Management Control – AICOGestión, Director of the Scientific Research Group of Strategic Cost Management Spain.

4Faculty of Medicine, National University of Colombia–, National Scientific Advisor Health and Life Sciences, Scientific Vice President and Innovation Colsanitas Clinic Bogotá, Colombia.

Cite as: Dueñas Casallas R, Crespo Soler C, Ripoll Feliu VM, Álvarez Moreno CA. Management and efficiency in highly complex public healthcare: an analysis of financial ratios and non-parametric statistic. Data and Metadata. 2024; 3:.630. https://doi.org/10.56294/dm2024.630

Submitted: 11-06-2024 Revised: 13-09-2024 Accepted: 29-12-2024 Published: 30-12-2024

Editor: Adrián

Alejandro Vitón-Castillo ![]()

Corresponding author: Robinson Dueñas Casallas *

ABSTRACT

Introduction: the objective of the study was to evaluate the management and technical efficiency of public health, taking as a sample the 25 specialized public hospitals in Colombia as well as the data of their annual financial statements and income statements from 2017 to 2022.

Method: a total of 28 financial ratios were developed for each hospital and year, then a correlation test was carried out, selecting nine of the best results to determine those with the greatest contribution to the data and their changes. To evaluate the management and technical efficiency, the SPSS and R software were used for the statistical analysis.

Results: according to Kruskall-Wallis’ test, they do not have technical efficiency, the results are below average and mostly negative, which allowed identifying opportunities for improvement of the financial and operational management systems, efficiency and productivity. Therefore, the research hypothesis is rejected.

Conclusion: there is no technical efficiency in the hospitals analyzed, high degrees of management asymmetry are observed in most of the ratios analyzed, there are possibilities of operational and financial risk, hence it is suggested to enhance management control, and thereby some recommendations and new research are given.

Keywords: Management; Efficiency; Public Health; Financial Indicators; Hospitals.

RESUMEN

Introducción: el objetivo de estudio fue evaluar la gestión y eficiencia técnica de la salud pública, tomando como muestra los 25 hospitales públicos especializados de Colombia y de data sus balances anuales de situación financiera y estados de resultados del 2017 al 2022.

Método: se elaboraron 28 ratios financieros para cada hospital y año, luego una prueba de correlación, seleccionando nueve de los mejores resultados para determinar aquellos con mayor contribución, finalmente un análisis de componentes principales (PCA), reduciendo la dimensionalidad, e identificando los de mayor influencia explicativa de la data y sus cambios. Para el análisis estadístico, evaluar la gestión y eficiencia técnica se usó los softwares SPSS y R.

Resultados: según el test de Kruskall – Wallis no tienen eficiencia técnica, los resultados están por debajo de la media y negativos en su mayoría, esto permitió identificar oportunidades de mejora de los sistemas de gestión financiero y operativo, eficiencia, y productividad y se rechaza la hipótesis investigativa.

Conclusión: no hay eficiencia técnica en los hospitales analizados, se observan altos grados de asimetría de gestión en la mayoría de los ratios analizados, hay posibilidades de riesgo operacional y financiero por lo que se sugiere potencializar el control de gestión, se dan algunas recomendaciones y nuevas investigaciones.

Palabras clave: Gestión; Eficiencia; Sanidad Pública; Indicadores Financieros; Hospitales.

INTRODUCTION

Management control in hospitals includes several organizational processes from the administrative and strategic to the assistance of medical services, seeking efficiency and profitability in diagnosis and treatment,(1) in this case the financial ratios are key to determine their economic position.(2) In Colombia and several developing countries, health systems face crises, which requires optimizing resources and evaluating the economic health and efficiency of health entities for the best decisions on growth and projection.(3)

Studies are needed to both reveal the financial status of public hospitals and provide a prospective overview that allows for timely and effective improvement measures to be taken,(4,5) and in turn promote an optimal and viable health system where the use of public resources is their best calling card and leverages growth and quality of life

Prior to this study, the authors of the current research, a bibliometric and systemic analysis with the Proknow-C methodology, which identified gaps in accounting and management control in healthcare, such as the use of financial ratios and efficiency in hospitals. For this reason, this research evaluated the financial health and technical efficiency of public hospitals in Colombia through financial ratios and non-parametric statistics.(6) Different tests and trials were applied to obtain the results and compare them, providing tools to improve the indicators and align them with SDG 3 on Health and Well-being of the 2030 agenda and offering reflections for public health policies.

The results showed the technical inefficiency of the hospitals studied, which, according to the contrasts made in this study, may have their origin years ago as a consequence of a deficient internal management control by the entity and external by the control and surveillance entities. Some guidelines were given to improve the use of public resources in the health sector and thus improve the quality of health care and improve the quality of life.

METHOD

A non-experimental-trans-sectional design was used with a synthetic analytical method, of a documentary-exploratory-descriptive type. This study included a selection of 25 high complexity and/or third level hospitals from a total of 931. The selection was based on characteristics, services, infrastructure, scientific research and budget allocation. The data were provided by the Ministry of Health and Social Protection of Colombia (widely known as Minsalud), including financial statements and annual income statements from 2017 to 2022, which issued Resolution 1441 of 2013 regulating the patrimonial and financial sufficiency of health entities.(7)

The distribution and normality of the data were evaluated,(8) using Kolmogorov-Smirnov and Shapiro-Wilk tests, finding that several ratios did not follow a normal distribution. To manage heterogeneity, robust approaches and adjustments were applied, in addition to a correlation test with the Pearson coefficient,(9) selecting the best nine results (see table 1).

Where:

rij It is the relationship between two indicators.

n is the number of observations.

Xi, Xj are the values belonging to both indicators.

|

Table 1. Principal Component Analysis (PCA) for the Selection of Financial Indicators |

|||||||||

|

Ratios or Indicators |

Debt ratio |

Debt asset |

Roa |

Roe |

Ebitda |

Collection rotation period |

Doubtful accounts |

Operating cycle |

Net operating working capital |

|

Debt ratio |

1 |

-0,30576618 |

0,023249414 |

-0,848819427 |

-0,166868588 |

0,001146575 |

-0,184958949 |

0,010583564 |

0,090998539 |

|

Debt asset |

-0,30576618 |

1 |

-0,015541085 |

0,234278503 |

0,10049769 |

-0,003168202 |

0,691818947 |

-0,045634567 |

-0,325620121 |

|

Roa |

0,023249414 |

-0,015541085 |

1 |

0,467106005 |

0,043752428 |

0,062822483 |

0,0808521 |

-0,965554202 |

0,202815731 |

|

Roe |

-0,848819427 |

0,234278503 |

0,467106005 |

1 |

0,128752718 |

0,031791925 |

0,111793615 |

-0,488143787 |

0,009520853 |

|

Ebitda |

-0,166868588 |

0,10049769 |

0,043752428 |

0,128752718 |

1 |

0,138509753 |

0,134494429 |

-0,031004656 |

-0,457536753 |

|

Collection rotation period |

0,001146575 |

-0,003168202 |

0,062822483 |

0,031791925 |

0,138509753 |

1 |

-0,042220367 |

-0,01973436 |

-0,08459094 |

|

Doubtful accounts |

-0,184958949 |

0,691818947 |

0,0808521 |

0,111793615 |

0,134494429 |

-0,042220367 |

1 |

-0,068504345 |

-0,100252815 |

|

Operating cycle |

0,010583564 |

-0,045634567 |

-0,965554202 |

-0,488143787 |

-0,031004656 |

-0,01973436 |

-0,068504345 |

1 |

-0,140147033 |

|

Net operating working capital |

0,090998539 |

-0,325620121 |

0,202815731 |

0,009520853 |

-0,457536753 |

-0,08459094 |

-0,100252815 |

-0,140147033 |

1 |

The PCA identified the highest contributing ratios, maximizing the variance through orthogonal components. The proportion of variance explained by each component was calculated as follows.

![]()

Where it represents the eigenvalue associated with component i.

The contributions of each variable in the first three principal components (PC1, PC2 and PC3) were observed:

1. Principal Component 1 (PC1): captures 28,96 % of the variance. Most important variables: ROE (0,537), Operating cycle (0,440), ROA (0,425).

2. Principal Component 2 (PC2): captures 23,02 % of the variance. Most important variables: Net operating working capital (0,442), ROA (0,440), Debt asset (0,431).

3. Principal Component 3 (PC3): captures 14,44 % of the variance. Most important variables: EBITDA (0,582), Collection turnover period (0,468), Operating net working capital (0,452).

Based on the results, indicators were selected that have a high load (in absolute value) in at least one of the first three principal components:

1. ROA: important in PC1 and PC2.

2. Net operating working capital: high contribution in PC2 and PC3.

3. Operating cycle: High contribution in PC1 and relevant in PC2.

ROA: key indicator that explains the variance in the first two components, suggesting that it is a good reflection of the overall performance of the entities analyzed. Net operating working capital: appears in components PC2 and PC3, highlighting its importance in the variability of working capital management data. Operating cycle: complements the three previous ones, highlighting operational efficiency. The statistical analysis was performed with SPSS and R software, allowing the evaluation of its management and efficiency using financial data.

Hypothesis Statement

Null hypothesis: = the hospitals in the study have a management model that allows for their technical efficiency, according to the different ratios analyzed.

![]()

Being:

• H0 Null hypothesis.

• Gifn Financial indicator n.

Alternative hypothesis = the hospitals in the study do not have a management model that allows for their technical efficiency, according to the different ratios analyzed. Obtaining:

![]()

Being:

• H1 Alternative hypothesis.

• Gifn Financial indicator n

Finally, the degree of technical efficiency in the financial management of hospitals is calculated using Kruskall-Wallis’ test, equivalent to the ANOVA test, determining whether to reject the null hypothesis or accept the alternative hypothesis, considering the statistical hypothesis as follows:

![]()

Theoretical framework

The World Health Organization (WHO) points out that United Nations countries must increase funding for their health systems to ensure universal access and coverage. A study by the WHO and the OECD indicates that there are no models applicable to all countries, due to their differences.(10) In Colombia, most third-level hospitals are located in the capital and economically relevant cities.

Hospitals assess their economic and financial situation through the balance sheet and the income statement, which are related to efficiency. Giner & Abásolo(11) emphasize the need to analyze financing in public health. The Covid-19 pandemic has highlighted the importance of financial management control in the crisis, supported by a study on the profitability and financial planning of health entities.(12) In turn, hospitals are classified by their assets and level of care, which affects their efficiency(13) and according to their specialty offered, their profit;(14) non-profit hospitals must maximize resources, supported by studies that link GDP and their size. (15,16,17)

According to Ali et al.,(18) ratios are essential to evaluate the efficiency and benefit of organizations, analyzing leverage, accounts receivable turnover rates among others.(19) ROA, ROE and market;(20) quality and efficiency,(21) policy and essence of the health service;(22) performance measurement with indicators of the lines of action financial, internal, customer and learning and growth of the Balanced Scorecard.(23) Figure 1 illustrates the distribution of high complexity public hospitals in Colombia.

Figure 1. High complexity public hospitals in Colombia

Siedlecki(24) indicates that access to health services depends on the size and location of the population; in the case of Colombia, the Amazon and Orinoquia do not have high complexity hospitals despite their large size.

RESULTS

For the analysis of the ratios, histograms, bar charts, pilot box and qq plot were created, unified by KPI in a single figure.

ROA – Return on Assets

An entity’s ability to generate profit on assets is measured by ROA. A high ROA reflects effective management and significant profit generation with few assets. Figure 2 shows representations of this ratio.

Figure 2. ROA – Return on assets

Hospitals have a mean of -14,063 % and a standard deviation of 7,913 % return, a range between -47,755 % as minimum and -6,872 % as maximum. It has negative asymmetry equivalent to -3,42 points with a bias to the left and a leptokurtic kurtosis of 14,36 points, indicating a high degree of concentration of data with an atypical value (Outliers). In 2019 it had total assets of $217,261 million and in 2022 the amount rose to $321,866 million, with a growth of 48 % in three years, due to the acquisition of technologies, the opening of the El Limonar headquarters and the launch of new services.(25)

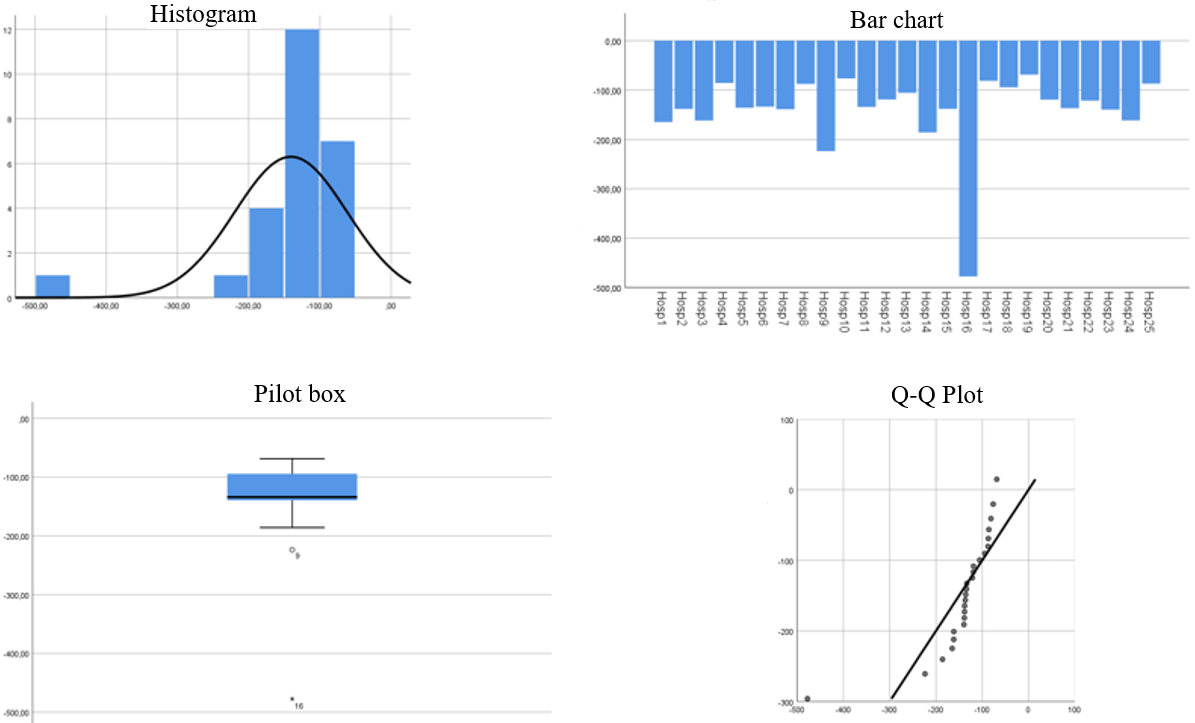

Operating cycle

It is the average time (days) to receive income for their services, including copayments, traffic accidents, private and prepaid medicine; necessary to improve the quality of health services, as shown in figure 3.

Figure 3. Operating cycle

This ratio has a mean of 228,04 days, a standard deviation of 466,63 days and a range of 52,45 days as minimum value and 2420,65 days as maximum. A high positive right skewness equals 4,684 points, a leptokurtic kurtosis of 22,687 points. Except for hospitals 6, 10 and 16, the values start at 53 days for the collection of services.

Net operating working capital

These are economic resources necessary for the operation of an entity; a high result indicates a greater need for cash, which is not favorable for an organization. Figure 4 shows the behavior of hospitals with respect to this ratio.

Figure 4. Operating net working capital

Hospitals have an average of $113 429 881 779,31, standard deviation of $74 445 233 345,98, range of action with a minimum of $5 650 955 541,17 and a maximum of $310 336 615 405,67 showing extreme and very different values from each other, belonging to hospitals 9 and 4 (outlier). A positive asymmetry equivalent to 0,991 points with a tendency to the right and a kurtosis that reaches 0,929 points of a leptokurtic nature is observed, implying a high concentration of data to the left of the distribution.

The results of hospitals 4 and 9 have extreme magnitudes, for example, the health service benefits account 1319, in 2022, hospital 4 had $486 775 562 481 evidenced by its care to the migrant population and hospital 9, $119 744 164 589. In table 2, the nine most representative ratios of the 28 facts identify weak points and areas of inefficiency in resource management.

|

Table 2. Descriptive statistics |

|||||||||

|

Financial Ratios |

N |

Minimum |

Maximum |

Average |

Std. Deviation |

Asymmetry |

Kurtosis |

||

|

Statistical |

Statistical |

Statistical |

Statistical |

Statistical |

Statistical |

Std. Error |

Statistical |

Std. Error |

|

|

Net Operating Working Capital |

25 |

5 650 955 541,17 |

310 336 615 405,67 |

113 429 881 779,31 |

74 445 233 345,98 |

0,991 |

0,464 |

0,929 |

0,902 |

|

Total Debt |

25 |

-232 268 |

102 615 |

10 759 |

65 141 |

-2 762 |

0,464 |

8 936 |

0,902 |

|

Debt Asset |

25 |

4 291 |

130 519 |

26 940 |

28 621 |

2 710 |

0,464 |

7 750 |

0,902 |

|

ROA |

25 |

-477 554 |

-68 724 |

-140 634 |

79 133 |

-3 423 |

0,464 |

14 366 |

0,902 |

|

ROE |

25 |

-561 137 |

205 306 |

-148 103 |

137 483 |

-0,039 |

0,464 |

4 630 |

0,902 |

|

EBITDA |

25 |

- 810 810 098 403,83 |

- 45 789 680 086,17 |

- 360 858 840 461,19 |

216 956 215 610,84 |

-0,629 |

0,464 |

-0,539 |

0,902 |

|

Collection rotation period |

25 |

2 593 |

2241 031 |

112 589 |

449 945 |

4 792 |

0,464 |

23 398 |

0,902 |

|

Doubtful accounts |

25 |

0,000 |

2 150 |

0,359 |

0,436 |

3 109 |

0,464 |

12 106 |

0,902 |

|

Operating Cycle |

25 |

52 453 |

2420 648 |

228 049 |

466 639 |

4 684 |

0,464 |

22 687 |

0,902 |

The hospitals studied have a chi-square distribution with k-1 degrees of freedom and using a significance level of 5 % (P-Value) or confidence level of 95 %, it is postulated that the H statistic is equivalent to 5 992, therefore, all those ratios greater than 5 % have a financial management model that establishes that there are no statistically relevant differences between the technical efficiency of the financial ratios and the study hospitals. According to the result of the Kruskal Wallis test presented in Table 3 and according to the statistical hypothesis:

![]()

It is inferred that only 1 of the 28 financial ratios developed at the beginning of the study for third-level hospitals in Colombia, that is, 3 %, statistically establishes technical efficiency associated with hospital management, while in 97 % of them it does not.

|

Table 3. Kruskal-Wallis’ test |

|

|

Indicator |

p_value |

|

Working capital |

0,000000000000000288021966113534 |

|

Net operating working capital |

0,0000000000000119869115232232 |

|

Cash cycle |

0,0000000000124005124745919 |

|

Operating cycle |

0,00000000000345845351317008 |

|

Debt asset |

0,000000000000000962881594339263 |

|

Dupont |

0,000000000000735235490100482 |

|

EBITDA |

0,000000000000000163365284048912 |

|

Estimate of difficult debt collection (doubtful accounts) |

0,0000000000471180331147217 |

|

Current liquidity |

0,000000000000130031290534256 |

|

Gross margin |

0,000000000000000173598651707605 |

|

Net margin |

0,00000000537871964235399 |

|

Operating margin |

0,00000000950326993468544 |

|

Financing period |

0,0000000000232622164299363 |

|

Collection rotation period |

0,0000000000000231178597722269 |

|

Payment rotation period |

0,0000000000000931928424975573 |

|

Debt quality ratio (short-term debt) |

0,0000000000000106310016589061 |

|

Availability ratio (absolute liquidity) |

0,00000000104326599289144 |

|

Debt ratio (total debt) |

0,00000000000861310190450429 |

|

Cash ratio (acid ratio) |

0,000000000000237317867626783 |

|

Long-term debt ratio |

0,0000000000000106310016589061 |

|

Debt of equity Ratio * |

0,461597333063618* |

|

Gross profitability on sales |

0,0000000000484612842663413 |

|

Net return on sales |

0,000000010761704707822 |

|

Return on investment (ROA), return on assets |

0,0000000000000596634603311261 |

|

Return on equity (ROE), return on equity |

0,000000000000735235490100482 |

|

Collection rotation |

0,0000000000000231178597722269 |

|

Inventory Turnover |

0,0000000000672252584536067 |

|

Payment rotation |

0,0000000000000931928424975573 |

DISCUSSION

The objective of the study was to evaluate the management and technical efficiency of public health, taking as a sample the 25 specialized public hospitals in Colombia as well as the data of their annual financial statements and income statements from 2017 to 2022.

The results showed the technical inefficiency of the hospitals studied, which, according to the contrasts made in this study, may have their origin years ago as a consequence of a deficient management control by the hospitals and by the control and surveillance entities, an example of this is the multiple interventions of Supersalud and their results.

ROA – Return on assets

In this ratio the negative amounts are striking, denoting opportunities for improvement in the use of public resources. The hospital 16 presents an underutilization of assets or its capacity could be insufficient for the demand, requiring a study on its productivity and efficiency improvement. This is in line with the study by Meredith JO et al.(4), which suggests that this can be improved by opting for process standardization. The results of the ROA ratio can affect investment in research, technologies and strategies such as public-private alliances (PPA); therefore, an improvement plan is necessary to ensure hospitals’ financial viability, and an improvement plan is needed to ensure the financial viability of hospitals. This finding is in line with several articles(33,34), such as the study by a National Accounts at a Glance.(35) Furthermore, it is important to underline that the hospital 16, since 2018, has been under the intervention of the National Health Superintendence (Supersalud), increasing its assets largely through State action.

The triangulation of results with news publications from the hospital confirms the findings of this study. It is important to evaluate management control due to the impact of the pandemic on assets, as Lee M,(2) study states, financial ratios help to show the economic and financial position of hospitals. It is suggested to take advantage of new technologies acquired in scientific and academic research alliances at national and international level.

Operating cycle

For most hospitals, except 6, 10 and 16, this ration indicates that the collection of services starts on the 53 days, suggesting problems in resource management. This reality can be improved with the implementation of strategies that include both optimizing delivery service times, quality indices and inventory turnover, and improving the cash cycle, which has a positive impact on staff recruitment, payment of obligations and updating of medical equipment. This improvement is in accordance with the suggestions of the study carried out by Mannion R,(22) study. It should be noted that a report from the newspaper El Cronista,(26) indicates that the hospital 16 was intervened in 2014 by Supersalud, due to a financial risk; however, in 2020 because of the Covid-19 pandemic, it optimized emergency and intensive care services, showing an improvement in the management control system.

Net operating working capital

This indicator shows that 56 % of hospitals require significant funds to respond to the needs of the population, suggesting a thorough review related to their technical efficiency. In this sense, a recommendation for the directors of health entities is to strive for a financial reorganization that allows operational viability and institutional strengthening. This suggestion is in line with those found in the study carried out by Purbey S, et al.(31), which entail efficiency, effectiveness and flexibility.

According to Arístides Hernández, a union leader of Asintraser Salud Norte, hospital 4 has a debt of more than $80 000 000 000 for care to the population, a total loss of more than $900 000 000 for expired medications and accounts receivable have exceeded the limits.(27) On the website of hospital 4, in the transparency link, there is information on the monitoring of the 2020 action plan, which was not fulfilled by the financial area, confirming the results of this study and the need for improvement and restructuring plans.(28) The above shows that there are undesired results in the performance measurement process, as it is addressed in the study performed by Mannion R, Goddard.

The hospital 9 was intervened by Supersalud in 2022, and in 2023, a special surveillance order was issued due to management problems and potential risks.(29) The results of this ratio suggest improving portfolio, debtors and inventory management and thus protecting cash flow, inventory and portfolio rotations, hard-to-collect ratios, minimizing financial costs and storage, deterioration and maturity expenses. Regarding this finding, Popesko B, et al.(1) in his study shows that hospital efficiency is associated with the applicability of a correct management control of these aspects. Therefore, the hospitals as a whole should internalize and apply these principles in their care and administrative processes.

CONCLUSIONS

The research hypothesis that states that third-level public hospitals in Colombia have a management model that demonstrates technical efficiency is rejected. High degrees of management asymmetry are observed in most of the ratios analyzed, along with high variability in kurtosis and dispersion, related to the results of the study, inferring that there is a high degree of operational risk, minimization of profit, expected efficiency and financial imbalance that generate internal vulnerability to exogenous health variables such as the pandemic. For this reason, technology, innovation and adequate management control of resources will improve care, treatment success and quality of patients’ life.(30)

Hospitals 4, 6, 8, 9, 16 and 18 are the most frequent outliers in the study, with financial trends that need to be evaluated to determine their impact and consequences that allow for the establishment of improvement plans, process restructuring and the establishment of short, medium and long-term goals and objectives. This is contrasted with the standard deviation of the ratios analyzed, which indicates high degrees of amplitude and negative values, suggesting heterogeneity in hospital management models, which is not a determinant of problems, but could be useful for analyzing management and establishing optimal and empirical KPIs of efficiency. Purbey et al.(31) conclude that the criteria for measuring performance are divided into three categories. Efficiency: appropriate use of economic resources with respect to the services provided with social responsibility towards stakeholders.(32) Effectiveness: quality of service, customer satisfaction and growth and Flexibility: adaptability and evaluation of the environment.

The negative results below the average raise the need to review the financial management systems and models and even intervention of Supersalud before considering the unfeasibility of them. During the Covid pandemic, health demand grew exponentially, causing a care crisis that required immediate responses, generating uncertainty about the financial preparation of health systems and their policies, given that even developed countries collapsed due to overdemand. Therefore, the claim of increased hospital income and profitability for the care of Covid patients is incorrect. Similarly, at a global level, health represents a significant percentage of national spending, especially after the pandemic, according to the OECD, and it should include medical equipment and outpatient services in public health, research and development.(33)

Limitations

Data availability is one of the limitations of this study because although the International Public Sector Accounting Standards (IPSAS) is applied, there is no standard for presenting information, which makes it difficult to categorize and organize data. The results are only comparable with high-complexity hospitals because level 1 and 2 hospitals were not taken into account.

Future studies

Further studies should analyze the installed capacity of each hospital, versus the population served; studies with other levels of care, analysis of health entities regarding the degree of related social impact, opportunity, quality, conditions of health personnel, infrastructure, Research, Development, Innovation and Creation – (R+D+I+C).

REFERENCES

1. Popesko B, Novák P, Papadaki Š. Measuring diagnosis and patient profitability in healthcare: Economics vs ethics. Economics and Sociology. 2015;8(1):234–45.

2. Lee M. Financial Analysis of National University Hospitals in Korea. Osong Public Health Res Perspect. 2015;6(5):310–7.

3.Creixans-Tenas J, Arimany-Serrat N. Influential variables on the profitability of hospital companies. Intangible Capital. 2018;14(1):171–85.

4. Meredith JO, Grove AL, Walley P, Young F, Macintyre MB. Are we operating effectively? A lean analysis of operating theater changeovers. Operations Management Research [Internet]. 2011;4(3):89–98. Available from: https://doi.org/10.1007/s12063-011-0054-6.

5. Banditori C, Cappanera P, Visintin F. A combined optimization–simulation approach to the master surgical scheduling problem. IMA Journal of Management Mathematics [Internet]. 2013 Apr 1;24(2):155–87. Available from: https://doi.org/10.1093/imaman/dps033.

6. Román P, Luis P. Technical efficiency of microenterprises financial ratios non-parametric intersectoral inferential statistical study San Bernardo Santiago. Capic Review 2017;15(2):109–22.

7.Ministry of Health and Social Protection. Resolution 1441. 2013; Available from: https://minsalud.gov.co/sites/rid/Lists/BibliotecaDigital/RIDE/DE/DIJ/resolucion-1441-de-2013.pdf.

8. Amaral M. Profitability of Commercial Banks in Portugal and Spain: A Panel Data Analysis Model | Profitability of Commercial Banks in Portugal and Spain: A Panel Data Analysis Model. Journal of Quantitative Methods for Economics and Business. 2024;(37):1–19.

9. Kalnins A, Praitis Hill K. Additional caution regarding rules of thumb for variance inflation factors: extending O’Brien to the context of specification error. Quality & Quantity 2024.

10. Barber SL, Lorenzoni L, Ong P. Price Setting and Price Regulation in Health Care [Internet]. OECD; 2019 [cited 2024 Nov 25]. Available from: https://www.oecd-ilibrary.org/social-issues-migration-health/price-setting-and-price-regulation-in-health-care_ed3c16ff-en

11. Giner R, Lorenzo A, Abásolo A. Financial analysis of hospital companies in the Canary Islands: a comparative study in Spain as a whole.2004;1-19.

12.Cortes-Romero A, Rayo Cantón S, Lara-Rubio J. An Explanatory-Predictive Model of the Financial Profitability of Companies in the Main Spanish Economic Sectors. 2011.

13. Bem A, Prędkiewicz K, Prędkiewicz P, Ucieklak-Jeż P. Determinants of Hospital’s Financial Liquidity. Procedia Economics and Finance [Internet]. 2014;12:27–36. Available from: https://www.sciencedirect.com/science/article/pii/S2212567114003177

14. Horwitz JR. Market watch: Making profits and providing care: Comparing nonprofit, for-profit, and government hospitals - Discussion of the value of nonprofit hospital ownership must account for the differences in service offerings among hospital types. Health Aff. 2005;24(3):790–801.

15. Bernabé Pérez MM, Sánchez Ballesta JP. The profitability of the Spanish company: A study of the nineties. Double entry [Internet]. 2002;131:98–111. Available from: https://portalinvestigacion.um.es/documentos/63c0b2ca3df4c204fbafd895

16. Vélez-González H, Pradhan R, Weech-Maldonado R. The role of non-financial performance measures in predicting hospital financial performance: The case of for-profit system hospitals. J Health Care Finance. 2011;38(2):12–23.

17.Turner J, Broom K, Elliott M, Lee J. A Decomposition of Hospital Profitability: An Application of DuPont Analysis to the US Market. Health Serv Res Manag Epidemiol 2015 Jul 22;2:2333392815590397–Dec

18. Mohd Ali M, Abu Bakar R, K Ghani E. The Effect of Firm Internal and External Characteristics on Risk Reporting Practices among Malaysian Listed Firms. Indonesian Journal of Sustainability Accounting and Management. 2018 Sep 7;2:107.

19. Singh JP, Pandey S. Impact of Working Capital Management on the Profitability of Hindalco Industries Limited. The IUP Journal of Financial Economics 2008;I(4):62–72.

20. Angori G, Aristei D, Gallo M. Determinants of Banks’ Net Interest Margin: Evidence from the Euro Area during the Crisis and Post-Crisis Period. Sustainability. 2019;11(14).

21. Alarussi AS, Alhaderi SM. Factors affecting profitability in Malaysia. Journal of Economic Studies [Internet]. 2018;45(3):442–58. Available from: https://EconPapers.repec.org/RePEc:eme:jespps:jes-05-2017-0124.

22. Mannion R, Goddard M. Performance measurement and improvement in health care. Applied Health Economics and Health Policy. 2002 Jan.

23. Kaplan R. Harvard Business Review. 1992. p. 71–6 The Balanced Scorecard—Measures that Drive Performance.

24. Siedlecki R, Bem A, Ucieklak-Jeż P, Prędkiewicz P. Rural Versus Urban Hospitals in Poland. Hospital’s Financial Health Assessment. Procedia - Social and Behavioral Sciences 2016;220:444–451.

25. Federico Lleras Hospital. Federico Lleras Acosta Hospital, three years of challenges. 2022.

26. The Chronicler. The 47th anniversary of the Federico Lleras Acosta Hospital. 2020.

27. Márquez J. Crisis at Erasmo Meoz University Hospital in Cúcuta could lead to mass layoffs. 2024.

28. Erasmo Meoz University Hospital. Action and development plan. 2021.

29. Rico S. ESE Caribbean University Hospital will be placed under special surveillance. 2023.

30. Dorfleitner G, Rößle F. The financial performance of the health care industry: a global, regional and industry specific empirical investigation. The European Journal of Health Economics [Internet]. 2018;19(4):585–94. Available from: https://doi.org/10.1007/s10198-017-0904-8

31. Purbey S, Mukherjee K, Bhar C. Performance measurement system for healthcare processes. International journal of productivity and performance management. 2007;56(3):241-51.

32. Valášková K, Gavurová B, Ďurana P, Mišanková M. Alter Ego Only Four Times? The Case Study of Business Profits in the Visegrad Group. E to M: Ekonomie to Management. 2020 Jan 1;23:101–19.

33. Reynaldos-Grandón KL, Rojas-Avila J. Administration models applied to care management: An approach to macro-, meso-, and micromanagement. Salud, Ciencia y Tecnología. 2024; 4:1173.

34. Alolayyan MN, Al- Daoud KI, Al Oraini B, Ahmmad Hunitie MF, Vasudevan A, Luo P, et al. Mathematical Model to Evaluate the Effect of Information Quality, and Management Capability on Hospital Performance. Salud, Ciencia y Tecnología. 2024;4:.979.

35. National Accounts at a Glance 2014 [Internet]. OECD; 2014 [cited 2024 Nov 22]. (National Accounts at a Glance). Available from: https://www.oecd-ilibrary.org/economics/national-accounts-at-a-glance-2014_na_glance-2014-en

FINANCING

From the Colombian Institute of Educational Credit and Technical Studies Abroad - ICETEX “Passport to Science Program - Scientific Colombia” in Focus: Country Society and from the Nueva Granada Military University in Colombia, entities where Dr. Robinson Dueñas was a beneficiary and is currently a professor.

ACKNOWLEDGEMENTS

To the anonymous referees for their valuable comments and suggestions, to Dra. Fernanda Cristina Pedrosa Alberto, from Coímbra Business School - ISCAC in Portugal and Dr. Luis Pedro Román Palma of the Universidad Central de Chile for his academic contributions; CP. Milton Franuel Urbano López, of the Directorate of Service Delivery and Primary Care of the Ministry of Health of Colombia for its technical data guidance; CP Mg Arnulfo Blanco Martínez for his technical data contributions; Statistician Kevin Steban Rodríguez Reyes for his professional contribution, to Ing. Fredy Agudelo Vargas for style review and readiness and Dr. José Marín Juanías, Professor of foreign languages, for editing guidance in the manuscript.

CONFLICT OF INTEREST

The authors declare that there is no conflict of interest.

AUTHORSHIP CONTRIBUTION

Conceptualization: Robinson Dueñas Casallas, Cristina Crespo Soler, Carlos Arturo Alvarez, Vicente Mateo Ripoll Feliu.

Data curation: Robinson Dueñas Casallas, Cristina Crespo Soler Vicente Mateo Ripoll Feliu.

Formal analysis: Robinson Dueñas Casallas, Cristina Crespo Soler, Carlos Arturo Alvarez, Vicente Mateo Ripoll Feliu.

Investigation: Robinson Dueñas Casallas, Cristina Crespo Soler, Carlos Arturo Alvarez, Vicente Mateo Ripoll Feliu.

Methodology: Robinson Dueñas Casallas, Cristina Crespo Soler, Vicente Mateo Ripoll Feliu

Project management: Robinson Dueñas Casallas, Cristina Crespo Soler, Vicente Mateo Ripoll Feliu.

Resources: Robinson Dueñas Casallas.

Software: Robinson Dueñas Casallas.

Supervision: Robinson Dueñas Casallas, Cristina Crespo Soler, Vicente Mateo Ripoll Feliu.

Validation: Robinson Dueñas Casallas, Cristina Crespo Soler, Carlos Arturo Alvarez, Vicente Mateo Ripoll Feliu.

Display: Robinson Dueñas Casallas, Cristina Crespo Soler, Vicente Mateo Ripoll Feliu.

Editorial – original draft: Robinson Dueñas Casallas, Cristina Crespo Soler, Vicente Mateo Ripoll Feliu.

Writing – review and editing: Robinson Dueñas Casallas, Cristina Crespo Soler, Carlos Arturo Alvarez, Vicente Mateo Ripoll Feliu.