doi: 10.56294/dm2024.681

ORIGINAL

Markov Switching Autoregressive in Information Systems for Improving Islamic Banks

Conmutación de Markov Autorregresiva en Sistemas de Información para Mejorar los Bancos Islámicos

Mahrus Ali1 ![]() *, Rahmat Gernowo2

*, Rahmat Gernowo2 ![]() *,

Budi Warsito3

*,

Budi Warsito3 ![]() *, Faliha Muthmainah4

*, Faliha Muthmainah4 ![]() *

*

1Diponegoro University, Doctoral of Information system department. Semarang, Indonesia.

2Diponegoro University, Physics department. Semarang, Indonesia.

3Diponegoro University, Statistics department. Semarang, Indonesia.

4State University of Malang, Psychology department. Malang, Indonesia.

Cite as: Ali M, Gernowo R, Warsito B, Muthmainah F. Markov Switching Autoregressive in Information Systems for Improving Islamic Banks. Data and Metadata. 2024; 3:.681. https://doi.org/10.56294/dm2024.681

Submitted: 25-06-2024 Revised: 30-09-2024 Accepted: 29-12-2024 Published: 30-12-2024

Editor:

Adrián

Alejandro Vitón Castillo ![]()

Corresponding Author: Mahrus Ali *

ABSTRACT

Sharia banks operate in several Muslim-majority countries, offering an alternative financial system aligned with Islamic principles. This study aims to develop a web-based information system for measuring the Maqasid Sharia Index (SMI) in real-time to assess the Islamization level of Sharia banks. Financial data from Indonesian sharia banks before and after their merger in 2021 (January 2013–February 2022) were analyzed. The Markov Switching Autoregressive (MSAR) method, with a margin of error of 0,107, was used to predict SMI values several years into the future. The results indicate that while the SMI value is predicted to decrease by 2025, the financial value of the banks is expected to increase. These findings provide valuable insights for improving the operational effectiveness of Sharia-compliant banking systems.

Keywords: Information System; Sharia Maqasid Index; MSAR; Improving Islamic Bank.

RESUMEN

Los bancos sharia operan en varios países de mayoría musulmana y ofrecen un sistema financiero alternativo alineado con los principios islámicos. Este estudio tiene como objetivo desarrollar un sistema de información basado en la web para medir el índice sharia maqasid (SMI) en tiempo real para evaluar el nivel de islamización de los bancos sharia. Se analizaron los datos financieros de los bancos sharia de Indonesia antes y después de su fusión en 2021 (enero de 2013-febrero de 2022). Se utilizó el método Markov Switching Autoregressive (MSAR), con un margen de error de 0,107, para predecir los valores del SMI varios años en el futuro. Los resultados indican que, si bien se prevé que el valor del SMI disminuya para 2025, se espera que el valor financiero de los bancos aumente. Estos hallazgos brindan información valiosa para mejorar la eficacia operativa de los sistemas bancarios compatibles con la Sharia.

Palabras clave: Sistema de Información; Índice Sharia Maqasid; MSAR; Mejora de la Banca Islámica.

INTRODUCTION

Based on the Royal Islamic Strategic Studies Center (RISSC) report entitled The Muslim 500: The World’s 500 Most Influential Muslims 2024, Indonesia is the country with the largest Muslim population in the world.

RISSC noted that the Muslim population in Indonesia will reach 240,62 million people in 2023. This number is equivalent to 86,7 % of the national population, which totals 277,53 million people. Pakistan ranks second in the country with the largest Muslim population after Indonesia, namely 232,06 million people or around 96,5 % of the country’s total population. Furthermore, India follows in third place with a Muslim population of 208,57 million people (14,6 %), Bangladesh 3,87 million people (91 %), and Nigeria 108,54 million people (48,5 %).

According to the RISSC report, the Vatican is the only country that does not have a Muslim population in the world. Meanwhile, the country with the smallest Muslim population in the world is Tokelau, with a population of less than 2 people or 0,1 % of its total population.

The following are the 10 countries with the largest Muslim populations in the world in 2023 according to the RISSC report accessed https://worldpopulationreview.com/country-rankings/muslim-population-by-country and Strong Islamic Bank 2023 accessed https://tabinsights.com/:

Fuente: (https://worldpopulationreview.com/country-rankings/muslim-population-by-country)

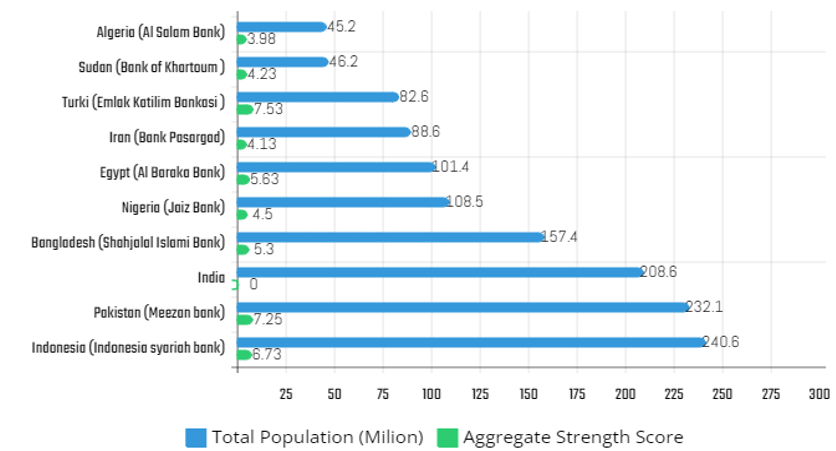

Figure 1. Comparison of population and health of Islamic banks

Based on figure 1, it shows that even though Indonesia has the largest Muslim population, the health of its Islamic banks is not growing as well as Turkey, which has a population of 82,6 million, but the health of its banks is much better. However, in the world of Islamic banking, total assets comply with sharia throughout the world (not including Iran) to grow by 12,8 % to $1,6 trillion in 2022, with 57 % held by stand-alone Islamic financial institutions, according to data from The Banker Database. The recorded growth is much higher than the banking sector as a whole, which experienced an asset contraction of 1,7 % in dollar terms in 2022.

As the country with the largest Muslim population in the world, Indonesia contributes 35 banks to the ranking of major Sharia banks in 2023, more than any other country. Sharia assets in the country fell 0,6 % in 2022, again due to the weak exchange rate of the rupiah against the dollar in that period. (World Population Review. Muslim Population by Country 2023 Available from: https://worldpopulationreview.com/country-rankings/muslim-population-by-country).

Bank Mandiri is Indonesia’s largest sharia lender in major rankings, in its role as the owner of Bank Syariah Indonesia (BSI), which was established by the government as the country’s leading sharia lender from the merger of three small lenders. BSI, whose asset base increased by 4,5 % in 2022, is now the largest non-Malaysian Islamic lender in Asia, overtaking IBBL in this year’s ranking. Apart from BSI, Islamic banks in Indonesia have been quite profitable this year, with 22 of the 35 banks recording an increase in assets, even though the rupiah exchange rate has weakened, this, therefore, shows the increasing demand for sharia-compliant banking services in this country. Based on figure 1, Indonesia’s Muslim population is the highest, but when discussing sharia-compliant assets, Indonesian state-owned Islamic banks are ranked 24th. The research results of(1) state that the merger of three Sharia banks consisting of Bank BRI Syariah, Bank BNI Syariah, and Bank Syariah Mandiri becoming an Indonesian Sharia Bank (BSI) has an impression on several parts, namely, banking, customers, workers, and society. For example, the impression on banking, the increase in banking capital resulting from the merger of three banks, increases economic activity in the field of sharia capital markets, and promotes the halal system in all service activities in banking.

Competition in the Indonesian Sharia banking market decreased drastically after the merger. Utami also found that although the previous BSI merger brought positive reactions in the stock market, BSI’s share price consistently declined after the merger. The research results of(1) and(2) are interesting to study because there is a gap in the condition of Indonesian sharia banks. Recently, a lot of research has been carried out regarding business cycle analysis in the banking industry. However, they mostly focus on the implications of macroeconomic changes on bank profitability. In addition, they send their findings as recommendations to management or policymakers, especially in the Islamic banking industry. Cihak et al.(3), Maximilian(4).

It is important to know about the prediction of bankruptcy and financial resource difficulties through the use of advanced data analysis and financial ratio indicators. It was concluded that this topic has not much been explored, there are few articles published in journals indexed in WoS, and therefore it is a good topic to investigate and innovate, for example, the inclusion of non-financial indicators.(5) For managers, good forecasts allow them to be aware of feasibility issues, so that strategies can be outlined to avoid bankruptcy and make accounting forecasts, increasing continuity and consistency at the same time, and avoiding manipulation.(6) Prediction models based on decision trees (or rules) allow easy identification of the causes of weak situations in which a person finds his company. On the other hand, concerning information users (e.g., investors, creditors, and banks), this model allows them to identify companies that tend to enter bankruptcy in order to make better investment and financing decisions.(7) These conditions trigger the presence of data mining and better predictions.(8,9)

This research aims to help depositors understand which macroeconomic variables have a significant influence on the volatility of customer returns at PT Bank Syariah Indonesia and then use these variables to predict future returns using Markov switching autoregressive calculations, namely the statistical model used to analyze time series data with the assumption that there are regime changes that occur stochastically. This model uses the Markov switching concept to describe changes in behavior or data dynamics over time. This method will be applied to a real-time information system. Any bank company can access it if they want to predict performance with the bank’s Shariah Maqasid Index in the future.

METHOD

In this section, the three components of the methodological approach are described in detail. First, the process of dividing the data set into a training set and an out-of-sample (testing) set is explained. Second, the data is analyzed through data science techniques and preprocessing steps. Third, the planning of the information system is carried out based on the results of data preprocessing.

Data Collection

We collected secondary data from the financial reports (annual reports) of Indonesian sharia banks which were uploaded on the company website https://www.bankbsi.co.id/, taken from January 2013 to February 2022, because this range represents the conditions before, during, and after Covid and represents state of the bank before the merger in 2021 and after the merger. The data taken is in the form of financial ratio values such as research, education, training, publications, profit equalization reserve, Mudharobah and musyarakah, non-interest income, zakat, assets, and real investment distribution according to the required SMI ratio.

Data preprocessing

The secondary data that has been taken contains duplicate data or empty rows which will later have an impact on data analysis. That’s why steps need to be taken until the data is ready to be tested in the system.

Step 1: Exploratory Data Analysis

This step is to check the structure of the data set, missing values, duplicates, and unique values of variables to analyze the way the data set is organized, there is a Pandas method that is run in Python like the following:

df.info()

There are no empty rows, meaning that all rows have been filled with data even though the data content is numeric 0. Next, test data duplication that there are no duplicate data between rows and columns except for the numeric 0.

Step 2: Deal with Missings

This step repairs the data if there is empty data in each row and column except for the value 0. However, because there are no rows and columns that have no value, there is no action in this step.

Step 3: Deal with Duplicates and Outliers

This step repairs the data if there is duplicate data in each row except the value 0. However, because no rows were found that had duplicate data, there is no action in this step.

Step 4: Encode Categorical Features

This stage is converting categorical features into numerical features. Because the data taken is all numeric data, there is no action at this step.

Information System Planning

The planning of this information system is carried out in stages based on science, such as creating a use case, manual calculation of the Sharia Maqasid index using reviews first before being applied to an online-based system because it will be compared from manual calculations or using tools into the information system whether the calculation results are the same or not and continued with future predictions with autoregressive markov switching.

Actors are users who will use this prediction system, for example, bankers, researchers and financial institutions who will predict the performance of Islamic banks. The user uploads a financial report according to the format created by the author, then enters the desired indicator variable data regarding the ratio that he wants to measure with the sharia maqasid index and at the same time the weight of the indicator that the company wants, then each indicator has a sub-indicator which is given a weight for each sub-indicator. After that, the sharia maqasid index calculation system will appear automatically in a matter of seconds, and the Markov switching autoregressive calculation is used to predict the company’s desired future for several years.

Sharia Maqasid Index calculation

The sharia maqasid index is an index used to measure the performance of sharia banks based on sharia maqasid. This index was developed by Mohammed (2008). He referred to Abu Zahrah’s maqasid sharia concept in the book of Usul Fiqh which was converted into financial ratios. Each element of the maqasid sharia index above has an average weight developed by Mohammed (2008). The average weight of the maqasid sharia elements is as follows: each element of the three objective concepts will be calculated using the formula applied in the application to the maqasid sharia index which is as follows:

The calculation results of each maqasid sharia index are added up using the following formula:

SMI = O1 + O2 + O3

Markov switching autoregressive

According to Hamilton (1989) the MSAR model is as follows:

yt = μSt + ϕ1(yt-1 - μSt-1) + ϕ2(yt-2 - μSt-2) + ϕ3(yt-3 - μSt-3) + ϕ4(yt-4 - μSt-4) + εt

And each period, the regime transitions according to the transition probability matrix as follows:

![]()

RESULTS

This information system is built from the Python, HTML and Javascript platforms which is run directly on the domain using a VPS (Virtual Private Server), but has not yet reached security as stated in the dimensions covered in the criteria of system effectiveness, system efficiency, compatibility, data security, and quality and safety.(17) The information system currently being built continues research from Farouk’s statement from his future research, namely the development of an information system for bank evaluation.(18) Therefore, this information system was built in which there is a standard measure of the Sharia Maqasid Index (Sharia bank size) which is calculated mathematically like Markov switching autoregressive which is also included in the system. The initial display when the URL address is called. In this display, the user enters financial reports for at least the last 5 consecutive years and has the extension .csv like the template provided by the system provider.

SMI calculation interface

Figure 5 has been completed perfectly, namely the final step to predict the value of the sharia maqasid index from the financial statements entered which will have an impact on future predictions of sharia banks. Table 1 explains the results of calculating the sharia maqasid index which is based on 01 related to human resource development, P02 related to justice, and 03 public interest.

|

Table 1. SMI calculation results |

||||

|

Month/Year |

O1 |

O2 |

O3 |

SMI |

|

Jan-13 |

110,976 |

5604,1752 |

2149,9411 |

0,79 % |

|

Feb-13 |

270,252 |

6051,1982 |

2294,8599 |

0,86 % |

|

Mar-13 |

429,672 |

6707,2146 |

2437,7342 |

0,96 % |

|

Apr-13 |

616,836 |

7262,4694 |

2546,4349 |

1,04 % |

|

Mei-13 |

748,944 |

7821,6028 |

2578,1029 |

1,11 % |

|

Jun-13 |

14,07 |

8530,7716 |

2725,6491 |

1,13 % |

|

Jul-13 |

17,565 |

9177,3006 |

2747,489 |

1,19 % |

|

Agu-13 |

19,86 |

9740,0666 |

2640,5805 |

1,24 % |

|

Sep-13 |

23,922 |

10350,1794 |

2732,7367 |

1,31 % |

|

Okt-13 |

27,486 |

11042,1938 |

2746,9786 |

1,38 % |

|

Nov-13 |

30,621 |

11643,7212 |

2701,7966 |

1,44 % |

|

………… |

………… |

………… |

………… |

………… |

|

Jan-22 |

241,074 |

323382,9408 |

181473,0854 |

50,51 % |

|

Feb-22 |

477,09 |

336355,8656 |

180817,5984 |

51,77 % |

In the information system, apart from being able to display a tabulation of sharia maqasid index calculations, the system can display graphs as in figure 2 to make it easier to analyze the fluctuations in SMI calculations over 10 years.

Figure 2. SMI graph

Based on figure 2, variable 02 is shown in yellow or is related to justice, the financing issued by banks is very high, and variable 01 is shown in blue or is related to human resource development, which is very low. It can be seen from the graph that this bank is experiencing 3 conditions, namely condition 1 bank before the merger, condition 2 banks being merged (during Covid-19), and condition 3 after the merger in 2022. In October 2020 (before the merger) this bank experienced a very significant increase. In 2021 (covid 19 conditions) there was a very low decline, but this decline experienced a very fast recovery as shown in the graph in 2022. Next, users will see the results of MSI debt as in the graphic image.

The results of the SMI calculation based on system show that between January and February, the performance based on SMI is the highest, meaning that when compared to figure 2, the higher the values of 01,02 and 03 will have an impact on the SMI value.

MSAR calculation prediction results

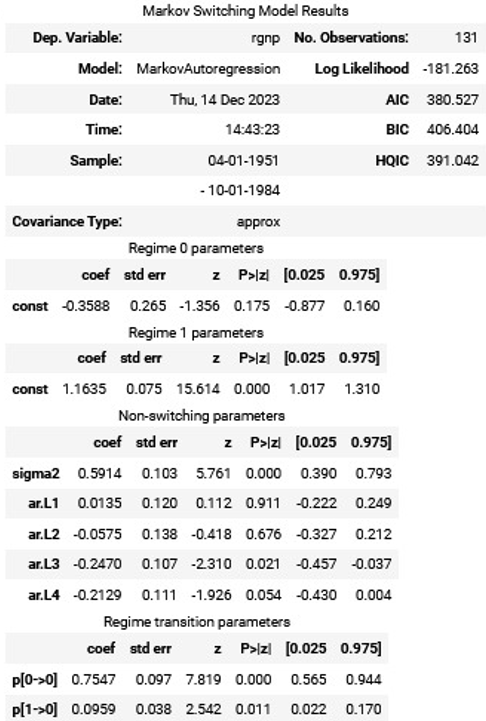

In this MSAR calculation, there are 2 regimes, namely the sharia regime whose SMI value is > 1 and the non-sharia (subhat) whose value is < 1. there is a factual SMI value (before it is predicted) and a predicted SMI value based on the uploaded data. The results of the MSAR calculation between the predicted value and the factual value have a lot of lines that coincide, which means the difference is small, the red color indicates the factual SMI value and the orange color is the prediction result, and it is explained in figure 3 that the regime value is 0 -0,3588 and in the regime 1 is worth 1,1635, meaning the lowest point of the subhat value in regime 0 and the highest value of sharia in regime 1.

Figure 3. Results of transition probability calculations

Figure 3 is a display of a Web-based information system being built. From this display, the transition probability is found which is used to calculate the condition of Islamic banks based on SMI in the next few years. The transition probability value is as follows:

![]()

If the transition probability value is used to predict the condition of Indonesian sharia banks in 2025, calculated from February 2022, if entered into the tabulation, the results are as follows:

|

Table 2. Transition probability values |

||

|

State |

State of next month (March 2022) |

|

|

Current month |

HALAL |

SUBHAT |

|

HALAL |

0,565 |

0,944 |

|

SUBHAT |

0,022 |

0,170 |

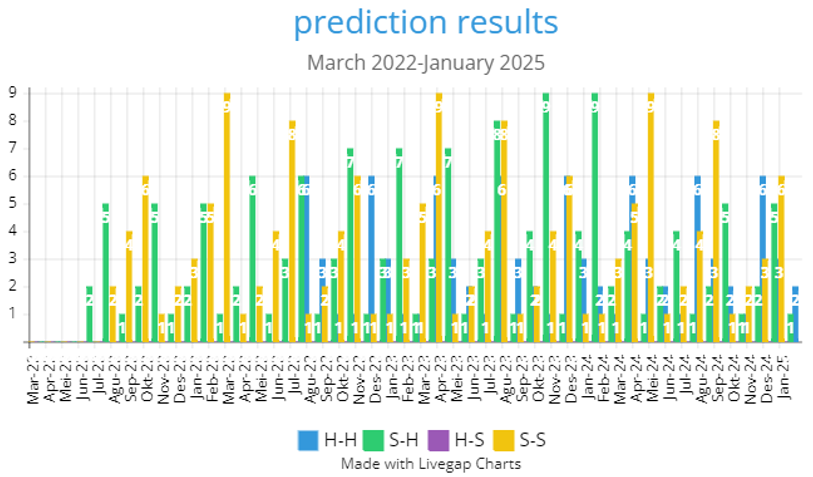

Based on table 2, we can calculate the condition of sharia bank SMI in 2025, whether halal or sub-hat, as in the following figure:

Figure 4. Predicted values from year to year

Information:

· H-H: Halal-Halal

· S-H: Subhat-Halal

· H-S : Halal – Subhat

· S-S: Subhat-subhat

In figure 4, it is explained that the sharia value is 2,22 x 10-12, which means the sharia value will decrease further, but when viewed from the Halal Subhat, the financial ratio will be healthier, worth 0,066632.

DISCUSSION

Ledhem’s experimental results(10) show that KNN and RF are effective techniques for predicting the financial performance of sharia banking in Indonesia. Based on metrics like MSE, RMSE, MAE, and R², KNN outperforms RF, making it the most suitable data mining technique for this purpose.(11,12,13) However, study does not explore long-term predictions or the application of other algorithms, focusing solely on sharia banks as research objects.(9,8)

Introduced a dynamic bankruptcy forecasting model equipped with parameters to compare past and present bankruptcies.(14,15,16) This framework relies on financial ratios, aligned with social systems theory, which emphasizes sustainability, teamwork, and governance in business models. However, Erdogan(14) framework does not incorporate sharia-specific performance measures like SMI or SCNP, limiting its relevance to Islamic banking.(17,18,16)

Reveal a strong correlation between management sentiment in annual reports and the financial performance of Islamic banks.(19,20,21,22) Positive sentiment is linked to improved performance, while negative sentiment, measured using inverse frequency document frequency, correlates with declines.(23,24) While insightful, Iqbal’s(25,26) study focuses on financial ratios and suggests future research should integrate machine learning and additional variables for a broader perspective.

Identifies the “Working Capital/Total Assets” ratio as critical for forecasting financial distress using traditional methods like the Altman Z-Score.(27,28,29) Additionally, “Standard Profit” and “Profit on Revenue” ratios are highlighted as key variables, supporting Basel Accord recommendations on bank capital risks. Comparatively, our research aligns total assets with variable 03 (public interest) but highlights minimal HR development as a limitation.

Despite these studies, most fail to address sharia-specific parameters and rely predominantly on financial ratios. They also lack predictive models for the future conditions of Islamic banks. This gap underscores the need for comprehensive approaches integrating sharia compliance measures and advanced predictive methods, particularly in forecasting the long-term performance of sharia banks.

CONCLUSIONS

The results of the experimental data entered by the tool of an information system built by the author himself show that the highest order of the sharia maqasid index variable is O2 or justice, and in second place O3 or public interest, and in third order O1 or human resource development, that is the prediction result. Indonesian sharia banks in 2025 when implemented in the information system. From this order, the weight of the sharia maqasid index for human resource development (O1) is 30 %, justice (O2) 41 %, and public interest (O3) 29 %. Based on research results, there is an inequality based on percentages, namely that O1 should be higher than O3, but in reality, the prediction results say O1 is much lower. This means that recommendations for Islamic bank management can increase human resources for their employees

BIBLIOGRAPHIC REFERENCES

1. H. Hersugondo, I. Ghozali, E. Handriani, T. Trimono, and I. D. Pamungkas, “Price Index Modeling and Risk Prediction of Sharia Stocks in Indonesia,” Economies, 2022, vol. 10, no. 1, pp. 1–13, doi: 10.3390/economies10010017.

2. I. Puspitasari, F. Utami, and I. K. Raharjana, “Determinants of Continuance Intention to Use Mutual Fund Investment Apps: The Changing of User Behavior during the Pandemic Crisis,” 2022. doi: 10.1109/BESC57393.2022.9995170.

3. J. Hesse, D. Malhan, M. Yalçin, O. Aboumanify, A. Basti, and A. Relógio, “An optimal time for treatment-predicting circadian time by machine learning and mathematical modelling,” Cancers (Basel), 2020, vol. 12, no. 11, pp. 1–32, doi: 10.3390/cancers12113103.

4. Y. Xu and U. Mansmann, “Validating the knowledge bank approach for personalized prediction of survival in acute myeloid leukemia: a reproducibility study,” Hum. Genet., 2022, doi: 10.1007/s00439-022-02455-8.

5. H. D. Shah, C. M. Bhatt, S. M. Patel, J. B. Khajanchi, and J. N. Makwana, “Churn prediction and fraud detection in dairy sector using machine learning,” in Handbook of Research on Records and Information Management Strategies for Enhanced Knowledge Coordination, Charotar University of Science and Technology, India: IGI Global, 2021, pp. 391–406. doi: 10.4018/978-1-7998-6618-3.ch023.

6. D. Ding, “Study on predictive model of financial distress based on rotation forest ensembles of support vector machines,” in Proceedings - 2020 International Conference on Wireless Communications and Smart Grid, ICWCSG 2020, pp. 343–347. doi: 10.1109/ICWCSG50807.2020.00079.

7. M. K. Ho, H. Darman, and S. Musa, “Stock Price Prediction Using ARIMA, Neural Network and LSTM Models,” in Journal of Physics: Conference Series, 2021, vol. 1988, no. 1. doi: 10.1088/1742-6596/1988/1/012041.

8. F. F. Ochoa Paredes, M. E. Chenet Zuta, S. W. Rios Rios, and A. J. Yarin Achachagua, “Decision-Making in Tourism Management and its Impact on Environmental Awareness,” Data Metadata, 2023, vol. 2, pp. 1–2, doi: 10.56294/dm202385.

9. A. A. Shlash Mohammad, I. A. A. Khanfar, B. Al Oraini, A. Vasudevan, S. I. Mohammad, and Z. Fei, “Predictive analytics on artificial intelligence in supply chain optimization,” Data Metadata, 2024,vol. 3, doi: 10.56294/dm2024395.

10. M. A. Ledhem, “Data mining techniques for predicting the financial performance of Islamic banking in Indonesia,” J. Model. Manag., 2022,vol. 17, no. 3, pp. 896–915, doi: 10.1108/JM2-10-2020-0286.

11. Y. Li, C. Stasinakis, and W. M. Yeo, “A Hybrid XGBoost-MLP Model for Credit Risk Assessment on Digital Supply Chain Finance,” Forecasting, 2022,vol. 4, no. 1, pp. 184–207, doi: 10.3390/forecast4010011.

12. C. Y. Lee, S. K. Koh, M. C. Lee, and W. Y. Pan, “Application of Machine Learning in Credit Risk Scorecard,” in Communications in Computer and Information Science, 2021, vol. 1489 CCIS, pp. 395–410. doi: 10.1007/978-981-16-7334-4_29.

13. W. Long, Z. Lu, and L. Cui, “Deep learning-based feature engineering for stock price movement prediction,” Knowledge-Based Syst., 2019, vol. 164, pp. 163–173, doi: 10.1016/j.knosys.2018.10.034.

14. I. Erdogan, O. Kurto, A. Kurt, and S. Bahtiyar, “A New Approach for Fraud Detection with Artificial Intelligence,” 2020. doi: 10.1109/SIU49456.2020.9302374.

15. Y. Alsaawy, A. Alkhodre, M. Benaida, and R. A. Khan, “A comparative study of multiple regression analysis and back propagation neural network approaches for predicting financial strength of banks: An Indian perspective,” WSEAS Trans. Bus. Econ., 2020,vol. 17, pp. 627–637, doi: 10.37394/23207.2020.17.60.

16. A. N. Berger, C. P. Himmelberg, R. A. Roman, and S. Tsyplakov, “Bank bailouts, bail-ins, or no regulatory intervention? A dynamic model and empirical tests of optimal regulation and implications for future crises,” Financ. Manag., 2022, doi: 10.1111/fima.12392.

17. P. Gemar, G. Gemar, and V. Guzman-Parra, “Modeling the sustainability of bank profitability using partial least squares,” Sustain., 2019,vol. 11, no. 18, doi: 10.3390/su11184950.

18. A. Gafni, G. S. Dite, E. S. Tuff, R. Allman, and J. L. Hopper, “Ability of known colorectal cancer susceptibility SNPs to predict colorectal cancer risk: A cohort study within the UK Biobank,” PLoS One, 2021,vol. 16, no. 9 September, doi: 10.1371/journal.pone.0251469.

19. J. Iqbal, M. K. Sohail, and M. K. Malik, “Predicting the future financial performance of Islamic banks: a sentiment analysis approach,” Int. J. Islam. Middle East. Financ. Manag., 2023,vol. 16, no. 6, pp. 1287–1305, doi: 10.1108/IMEFM-07-2022-0267.

20. G. Dash and B. Nayak, “An empirical study for customer relationship management in banking sector using machine learning techniques,” Int. J. Comput. Appl. Technol., 2022,vol. 68, no. 3, pp. 286–291, doi: 10.1504/ijcat.2022.124953.

21. A. Karas, “Russian bank data: Reasons of bank closure,” Data Br., 2020, vol. 29, doi: 10.1016/j.dib.2020.105343.

22. Machaca MH. Relationship between physical activity and quality of work life in accountancy professionals: A literature review. Edu - Tech Enterprise 2024;2:13–13. https://doi.org/10.71459/edutech202413.

23. M. Bayraktar, M. S. Aktas, O. Kalipsiz, O. Susuz, and S. Bayraci, “Credit risk analysis with classification Restricted Boltzmann Machine,” in 26th IEEE Signal Processing and Communications Applications Conference, SIU 2018, 2018, pp. 1–4. doi: 10.1109/SIU.2018.8404397.

24. Jacinto-Alvaro J, Casco RJE, Macha-Huamán R. Social networks as a tool for brand positioning. Edu - Tech Enterprise 2024;2:9–9. https://doi.org/10.71459/edutech20249.

25. F. Iqbal, A. Jaffri, Z. Khalid, A. MacDermott, Q. E. Ali, and P. C. K. Hung, “Forensic investigation of small-scale digital devices: a futuristic view,” Front. Commun. Networks, 2023,vol. 4, doi: 10.3389/frcmn.2023.1212743.

26. Fidel WWS, Cuicapusa EEM, Espilco POV. Managerial Accounting and its Impact on Decision Making in a small company in the food sector in West Lima. Edu - Tech Enterprise 2024;2:8–8. https://doi.org/10.71459/edutech20248.

27. K. Halteh, K. Kumar, and A. Gepp, “Financial distress prediction of Islamic banks using tree-based stochastic techniques,” Manag. Financ., 2018,vol. 44, no. 6, pp. 759–773, doi: 10.1108/MF-12-2016-0372.

28. Y. Hu, Z. Tao, D. Xing, Z. Pan, J. Zhao, and X. Chen, “Research on stock returns forecast of the four major banks based on ARMA and GARCH model,” 2020, vol. 1616, no. 1. doi: 10.1088/1742-6596/1616/1/012075.

29. J. Han and X. Zhu, “The two-layer SRU Neural Network Based Analysis of Time Series,” 2021, vol. 1952, no. 4. doi: 10.1088/1742-6596/1952/4/042098.

FINANCING

The authors did not receive financing for the development of this research.

CONFLICT OF INTEREST

The authors declare that there is no conflict of interest.

AUTHORSHIP CONTRIBUTION

Conceptualization: Mahrus Ali.

Data curation: Mahrus Ali.

Formal analysis: Mahrus Ali.

Research: Mahrus Ali.

Methodology: Mahrus Ali.

Project management: Mahrus Ali.

Resources: Rahmat Gernowo.

Software: Mahrus Ali.

Supervision: Rahmat Gernowo.

Validation: Budi Warsito.

Display: Mahrus Ali.

Drafting - original draft: Faliha Muthmainah.

Writing - proofreading and editing: Faliha Muthmainah.